Step into a world where the focus is keenly set on what does case a house mean. Within the confines of this article, a tapestry of references to what does case a house mean awaits your exploration. If your pursuit involves unraveling the depths of what does case a house mean, you've arrived at the perfect destination.

Our narrative unfolds with a wealth of insights surrounding what does case a house mean. This is not just a standard article; it's a curated journey into the facets and intricacies of what does case a house mean. Whether you're thirsting for comprehensive knowledge or just a glimpse into the universe of what does case a house mean, this promises to be an enriching experience.

The spotlight is firmly on what does case a house mean, and as you navigate through the text on these digital pages, you'll discover an extensive array of information centered around what does case a house mean. This is more than mere information; it's an invitation to immerse yourself in the enthralling world of what does case a house mean.

So, if you're eager to satisfy your curiosity about what does case a house mean, your journey commences here. Let's embark together on a captivating odyssey through the myriad dimensions of what does case a house mean.

Should i buy a home now or wait 2022 should i wait to buy a home in 2022 should you buy a home in a recession should you buy a home should you buy a house now should you buy a house in a recession should you buy an electric car should you buy a hybrid car should you buy bonds now should you buy twitter stock should you exercise when sick

Should You Buy a Home in 2022? Here's What You Need to Know

Should You Buy a Home in 2022? Here's What You Need to Know

This story is part of Recession Help Desk, CNET's coverage of how to make smart money moves in an uncertain economy.

After two years of a wildly hot and competitive housing market with skyrocketing home prices, there are some signs indicating that these record-high spikes might start leveling off. This past April, home price increases declined for the first time in four months, as did sales of new homes.

But many experts note that, given the ongoing shortage of properties, home prices will still continue to go up in 2022 -- just at a slower pace. Plus, prospective new homeowners have to contend with relatively high mortgage rates, which keep monthly mortgage payments expensive. Although mortgage rates have dropped slightly since the Federal Reserve announced its fourth rate hike of the year to continue combating inflation, they're still more than 2% higher than they were at the beginning of 2022. So homebuyers should expect their mortgage payments to be higher this year, even if lessening demand decreases competition for homes.

"If we've seen the peak in inflation then we have seen the peak in mortgage rates," said Greg McBride, chief financial analyst at CNET's sister site, Bankrate. "The outlook for a weaker economy will hold sway as long as inflation pressures begin to show evidence of easing. If we get a couple months down the road and that hasn't happened, then all bets are off."

Even though mortgage rates appear to be leveling off, when taking all of these factors into account, a homebuyer will now pay almost 47% more for the same property compared with a year ago, according to Realtor.com.

Buying a home is one of the most important money moves you'll ever make. It's an exceptionally personal decision that requires evaluating your long-term goals while making sure you're financially ready, from the down payment to interest on a home loan. Your job stability, household needs and the inventory available where you want to live all play a role in determining what makes sense for you.

Here are the most important things to consider when buying a house in 2022, including why it might make sense to wait or to rent instead of buy.

Key factors to consider when buying a home in 2022

Right now, home prices are still seeing double-digit growth nationwide and all-cash offers still make up around a quarter of housing bids, according to Jessica Lautz, vice president of demographics and behavioral insights at the National Association of Realtors. Does that mean you should try to hold off until prices start going down? Not necessarily.

The first thing to keep in mind is that expert predictions are imperfect. No one knows what's going to happen with the economy, even with warning signs for events like recessions. And timing the market, or trying to make decisions based on what you think will happen to prices or rates in the future, is generally not a sound strategy. "With housing, buyers tend to obsess over home values and how buying at a certain time may be better for appreciation and equity," said Farnoosh Torabi, personal finance expert and editor-at-large at CNET. "That's important, but your monthly housing payment is what really matters in the end."

Even if you have a plan, be prepared to pivot in this market. Maggie Moroney, 27, is trying to buy her first home in the Washington, D.C. area, but can't find anything affordable. Between sales and rentals, there's low inventory in both markets.

"I probably could try to buy something, but it'd be a little bit of a stretch, especially with interest rates," she said. Moroney doesn't want to rush the decision and plans to wait it out if she doesn't find a home she likes, with the hope that more inventory will start to hit the market. "I'd rather have a rental I'm not super in love with than a home I'm not in love with."

If you're teetering between buying a home and waiting, here are some factors to keep in mind.

1. Mortgage rates and price trends

In today's housing market, high prices along with home loan rates are two of the most important factors at play. Although mortgage rates fluctuate daily, they are expected to remain between 5-6% for the rest 2022 -- though what happens next with inflation will tell where rates are headed. So far, rates are already more than 2 percentage points higher than this time a year ago and passed the 5.5% mark in June, but seem to be evening out since the announcement of the Fed's fourth rate hike in July.

Although rates dipped slightly with the most recent interest hike, it's still important to understand how the rate you lock in for your mortgage will impact your monthly payments, as well as the total amount you'll pay over the lifetime of your loan.

For example, if you take out a 30-year fixed-rate mortgage to buy a $500,000 house at a 5.2% interest rate, you'll pay $488,000 in interest over the life of your loan. But if you wait and buy a $450,000 house at a 6.5% interest rate, you'll end up paying $574,000 in interest over the course of your mortgage. So even though you paid less for your home, you're paying more than the difference in price due to interest over three decades.

Scaling back your budget and looking at homes that may be smaller or in less-expensive neighborhoods is an option to consider if higher mortgage rates have made your previous housing goals unattainable.

2. Financial and personal goals

Homeownership is still considered one of the most reliable ways to build wealth. When you make monthly mortgage payments, you're building equity in your home that you can tap into later on. When you rent, you aren't investing in your financial future the same way you are when you're paying off a mortgage.

Another factor to take into consideration is how long you plan to live in the house. If you expect to live there for a decade or longer, you'll likely be able to refinance your mortgage to a lower rate, reducing your monthly payment in the process. However, if you plan to move in a few years, it likely won't make financial sense for you to refinance. In that case, it's worth considering an adjustable-rate mortgage, which can help offset today's high mortgage rates by offering you a lower initial interest rate that only adjusts or increases later on in your mortgage term.

3. Future housing trends and recession risks

As buyer competition decreases when buying a home becomes increasingly unaffordable, it could mean that inventory opens up where you're looking. In June, the national inventory of available homes grew by 18.7% this year compared to last year. More available inventory means that you have more homes to choose from, increasing the chances you can buy something you actually want this year versus scrambling in a bidding war for whatever is available in your budget.

But there's also talk of a looming recession. If you wait to buy instead, you could avoid potentially overpaying for a home that could lose its value in an upcoming economic downturn, said Torabi. Plus, if the economy slows down, it's possible the Federal Reserve will raise interest rates less aggressively, which could benefit potential homeowners trying to lock in a better rate on their mortgage.

Is it better to rent than buy right now?

It depends, especially when we're dealing with an unpredictable period of high inflation.

On one hand, if you buy a house and secure a fixed-rate mortgage, that means that no matter how much prices or interest rates go up, your fixed payment will stay the same every month. That's an advantage over renting since there's a good chance your landlord will raise your rent to counter inflationary pressures. Right now, rents are rising faster than wages, and if homebuyers are priced out of the housing market, there'll be more pressure to rent, which will increase competition. Many are already experiencing a red-hot rental market, leading to rental bidding wars and evictions.

On the other hand, even though a fixed-rate mortgage can offer you more predictability and budget stability, "as long as inflation continues to outpace wages, there could be benefits to renting right now as the economy worsens," said Torabi.

For example, one advantage of renting over buying is that you can save the cash you would have otherwise needed to use for a down payment. In a time of economic uncertainty, if you don't have to worry about coming up with a down payment and emptying most of your entire bank account to secure yourself a home, you can stay more liquid. Having more cash on hand can offer you added security if a recession negatively impacts your financial situation.

"It's important to know the differences in cost of owning a home versus the cost of renting," said Robert Heck, vice president of mortgages at Morty, an online mortgage marketplace. "How much is homeowners insurance going to cost? How much are the annual property taxes? Maybe you're not used to paying property taxes if you've been renting. Consider the costs that will go into maintaining a home."

Ultimately, whether you rent or buy often comes down to practical considerations like whether you need more space to start a family, or your lease is ending -- regardless of market conditions.

Should you buy a home in 2021 should you buy a home before selling should you buy a refurbished computer should you buy travel insurance should you buy tesla stock should you buy extended warranty should you pop a blister how many eggs should you eat

Should You Buy a Home in 2022? Here's What You Need to Know

Should You Buy a Home in 2022? Here's What You Need to Know

This story is part of Recession Help Desk, CNET's coverage of how to make smart money moves in an uncertain economy.

After two years of a wildly hot and competitive housing market with skyrocketing home prices, there are some signs indicating that these record-high spikes might start leveling off. This past April, home price increases declined for the first time in four months, as did sales of new homes.

But many experts note that, given the ongoing shortage of properties, home prices will still continue to go up in 2022 -- just at a slower pace. Plus, prospective new homeowners have to contend with relatively high mortgage rates, which keep monthly mortgage payments expensive. Although mortgage rates have dropped slightly since the Federal Reserve announced its fourth rate hike of the year to continue combating inflation, they're still more than 2% higher than they were at the beginning of 2022. So homebuyers should expect their mortgage payments to be higher this year, even if lessening demand decreases competition for homes.

"If we've seen the peak in inflation then we have seen the peak in mortgage rates," said Greg McBride, chief financial analyst at CNET's sister site, Bankrate. "The outlook for a weaker economy will hold sway as long as inflation pressures begin to show evidence of easing. If we get a couple months down the road and that hasn't happened, then all bets are off."

Even though mortgage rates appear to be leveling off, when taking all of these factors into account, a homebuyer will now pay almost 47% more for the same property compared with a year ago, according to Realtor.com.

Buying a home is one of the most important money moves you'll ever make. It's an exceptionally personal decision that requires evaluating your long-term goals while making sure you're financially ready, from the down payment to interest on a home loan. Your job stability, household needs and the inventory available where you want to live all play a role in determining what makes sense for you.

Here are the most important things to consider when buying a house in 2022, including why it might make sense to wait or to rent instead of buy.

Key factors to consider when buying a home in 2022

Right now, home prices are still seeing double-digit growth nationwide and all-cash offers still make up around a quarter of housing bids, according to Jessica Lautz, vice president of demographics and behavioral insights at the National Association of Realtors. Does that mean you should try to hold off until prices start going down? Not necessarily.

The first thing to keep in mind is that expert predictions are imperfect. No one knows what's going to happen with the economy, even with warning signs for events like recessions. And timing the market, or trying to make decisions based on what you think will happen to prices or rates in the future, is generally not a sound strategy. "With housing, buyers tend to obsess over home values and how buying at a certain time may be better for appreciation and equity," said Farnoosh Torabi, personal finance expert and editor-at-large at CNET. "That's important, but your monthly housing payment is what really matters in the end."

Even if you have a plan, be prepared to pivot in this market. Maggie Moroney, 27, is trying to buy her first home in the Washington, D.C. area, but can't find anything affordable. Between sales and rentals, there's low inventory in both markets.

"I probably could try to buy something, but it'd be a little bit of a stretch, especially with interest rates," she said. Moroney doesn't want to rush the decision and plans to wait it out if she doesn't find a home she likes, with the hope that more inventory will start to hit the market. "I'd rather have a rental I'm not super in love with than a home I'm not in love with."

If you're teetering between buying a home and waiting, here are some factors to keep in mind.

1. Mortgage rates and price trends

In today's housing market, high prices along with home loan rates are two of the most important factors at play. Although mortgage rates fluctuate daily, they are expected to remain between 5-6% for the rest 2022 -- though what happens next with inflation will tell where rates are headed. So far, rates are already more than 2 percentage points higher than this time a year ago and passed the 5.5% mark in June, but seem to be evening out since the announcement of the Fed's fourth rate hike in July.

Although rates dipped slightly with the most recent interest hike, it's still important to understand how the rate you lock in for your mortgage will impact your monthly payments, as well as the total amount you'll pay over the lifetime of your loan.

For example, if you take out a 30-year fixed-rate mortgage to buy a $500,000 house at a 5.2% interest rate, you'll pay $488,000 in interest over the life of your loan. But if you wait and buy a $450,000 house at a 6.5% interest rate, you'll end up paying $574,000 in interest over the course of your mortgage. So even though you paid less for your home, you're paying more than the difference in price due to interest over three decades.

Scaling back your budget and looking at homes that may be smaller or in less-expensive neighborhoods is an option to consider if higher mortgage rates have made your previous housing goals unattainable.

2. Financial and personal goals

Homeownership is still considered one of the most reliable ways to build wealth. When you make monthly mortgage payments, you're building equity in your home that you can tap into later on. When you rent, you aren't investing in your financial future the same way you are when you're paying off a mortgage.

Another factor to take into consideration is how long you plan to live in the house. If you expect to live there for a decade or longer, you'll likely be able to refinance your mortgage to a lower rate, reducing your monthly payment in the process. However, if you plan to move in a few years, it likely won't make financial sense for you to refinance. In that case, it's worth considering an adjustable-rate mortgage, which can help offset today's high mortgage rates by offering you a lower initial interest rate that only adjusts or increases later on in your mortgage term.

3. Future housing trends and recession risks

As buyer competition decreases when buying a home becomes increasingly unaffordable, it could mean that inventory opens up where you're looking. In June, the national inventory of available homes grew by 18.7% this year compared to last year. More available inventory means that you have more homes to choose from, increasing the chances you can buy something you actually want this year versus scrambling in a bidding war for whatever is available in your budget.

But there's also talk of a looming recession. If you wait to buy instead, you could avoid potentially overpaying for a home that could lose its value in an upcoming economic downturn, said Torabi. Plus, if the economy slows down, it's possible the Federal Reserve will raise interest rates less aggressively, which could benefit potential homeowners trying to lock in a better rate on their mortgage.

Is it better to rent than buy right now?

It depends, especially when we're dealing with an unpredictable period of high inflation.

On one hand, if you buy a house and secure a fixed-rate mortgage, that means that no matter how much prices or interest rates go up, your fixed payment will stay the same every month. That's an advantage over renting since there's a good chance your landlord will raise your rent to counter inflationary pressures. Right now, rents are rising faster than wages, and if homebuyers are priced out of the housing market, there'll be more pressure to rent, which will increase competition. Many are already experiencing a red-hot rental market, leading to rental bidding wars and evictions.

On the other hand, even though a fixed-rate mortgage can offer you more predictability and budget stability, "as long as inflation continues to outpace wages, there could be benefits to renting right now as the economy worsens," said Torabi.

For example, one advantage of renting over buying is that you can save the cash you would have otherwise needed to use for a down payment. In a time of economic uncertainty, if you don't have to worry about coming up with a down payment and emptying most of your entire bank account to secure yourself a home, you can stay more liquid. Having more cash on hand can offer you added security if a recession negatively impacts your financial situation.

"It's important to know the differences in cost of owning a home versus the cost of renting," said Robert Heck, vice president of mortgages at Morty, an online mortgage marketplace. "How much is homeowners insurance going to cost? How much are the annual property taxes? Maybe you're not used to paying property taxes if you've been renting. Consider the costs that will go into maintaining a home."

Ultimately, whether you rent or buy often comes down to practical considerations like whether you need more space to start a family, or your lease is ending -- regardless of market conditions.

Inflation interest rates and jobs how today stencile inflation interest rates and jobs how today weather inflation interest rates and jobs howard inflation interest rates and jobs howell inflation interest rates and jobs howey inflation interest rates and jobs howden inflation interest rates and recession inflation interest rate calculator inflation interest rates inflation interest rate relationship jimmy carter inflation interest rates inflation interest rate history

Inflation, Interest Rates and Jobs: How Today's Economy Compares to Recessions of the Past

Inflation, Interest Rates and Jobs: How Today's Economy Compares to Recessions of the Past

This story is part of Recession Help Desk, CNET's coverage of how to make smart money moves in an uncertain economy.

What's happening

There's still debate about whether the US economy is officially headed into a recession, but the economic downturn is causing widespread stress.

Why it matters

Periods of financial volatility and market decline can drive people to panic and make costly mistakes with their money.

What's next

Examining what's happening now -- and comparing it with the past -- can help investors and consumers decide what to do next.

Facing the aftershocks of a rough economy in the first half of 2022, with sky-high inflation, rising mortgage rates, soaring gas prices and a bear market for stocks, leading indicators of a recession have moderated slightly in the past month. That could mean the economic downturn won't be as long or brutal as expected.

Still, the majority of Americans are feeling the sting of rising prices and anxiety over jobs. The country has experienced two consecutive quarters of economic slowdown -- the barometer for measuring a recession -- even though the National Bureau of Economic Research hasn't made the "official" recession call.

At a time like this, we should consider what happens in a recession, look at the data to determine whether we're in one and try to maintain some historical perspective. It's also worth pointing out that down periods are temporary and that, over time, both the stock market and the US economy bounce back.

I don't mean to minimize the gravity and hardship of the times. But it can be useful to review how the economy has behaved in the past to avoid irrational or impulsive money moves. For this, we can largely blame recency bias, our inclination to view our latest experiences as the most valid. It's what led many to flee the stock market in 2008 when the S&P 500 crashed, thereby locking in losses and missing out on the subsequent bull market.

"It's our human tendency to project the immediate past into the future indefinitely," said Daniel Crosby, chief behavioral officer at Orion Advisor Solutions and author of The Laws of Wealth. "It's a time-saving shortcut that works most of the time in most contexts but can be woefully misapplied in markets that tend to be cyclical," Crosby told me via email.

Before you make a knee-jerk reaction to your portfolio, give up on a home purchase or lose it over job insecurity, consider these chart-based analyses from the last three decades. We hope this data-driven overview will offer a broader context and some impetus for making the most of your money today.

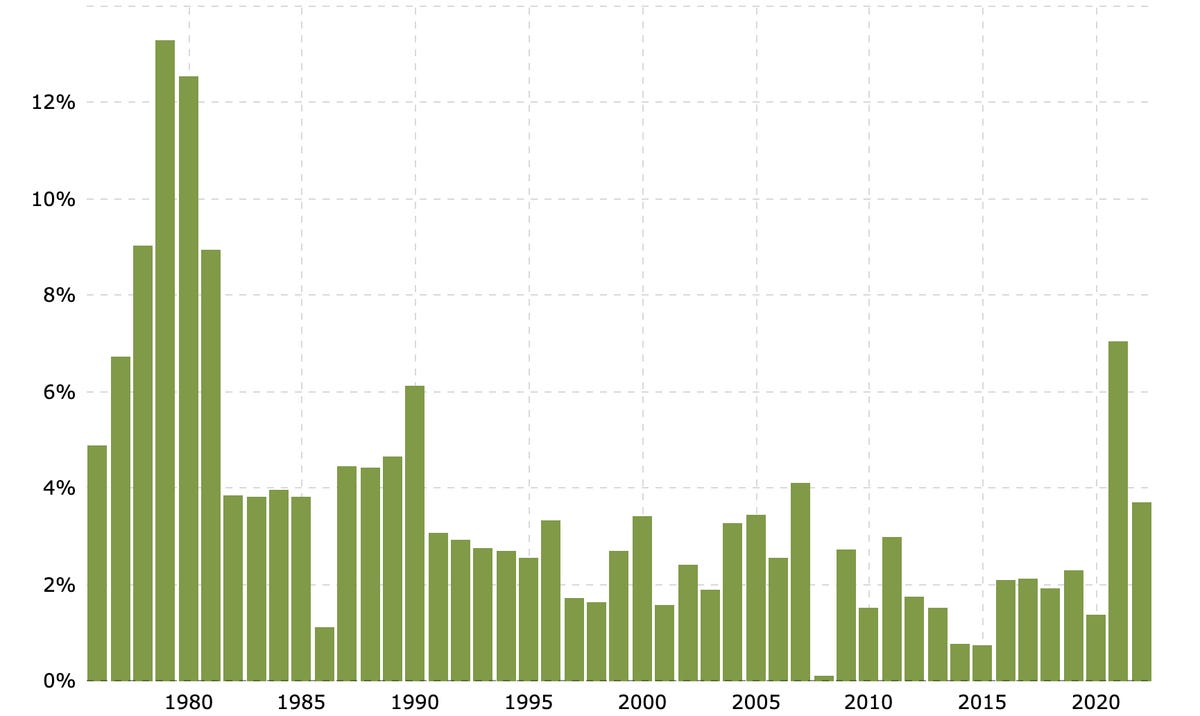

What do we know about inflation?

Historical inflation rate by year

Macrotrends.net

Current conditions: The US is experiencingthe highest rate of inflation in decades, driven by global supply chain disruptions, the injection of federal stimulus dollars and a surge in consumer spending. In real dollars, the 8.5% rise in consumer prices over the past year is adding about $400 more per month to household budgets.

The context: Policymakers consider 2% per year to be a "normal" inflation target. The country's still experiencing over four times that figure. The 9.1% annual rate in July was the largest jumpin inflation since 1980 when the inflation rate hit 13.5% following the prior decade's oil crisis and high government spending on defense, social services, health care, education and pensions. Back then, the Federal Reserve increased rates to stabilize prices and, by the mid-1980s, inflation fell to below 5%.

The upside: As overall inflation rates rise, the silver lining might be increased rates of return on personal savings. Bank accounts are starting to offer more attractive yields, while I bonds -- federally backed accounts that more or less track inflation -- are attracting savers, too.

What's happening with mortgage rates?

30-year fixed-rate mortgage averages in the US

Current conditions: As the Federal Reserve continues its rate-hike campaign to cool spending and try to tame inflation, the rate on a 30-year fixed mortgage has grown significantly. In June, the average rate jumped annually by nearly 3 percentage points to almost 6%. In real dollars, that means that after a 20% down payment on a new home (let's use the average sale price of $429,000), a buyer would roughly need an extra $7,300 a year to afford the mortgage. Since then, rates have cooled a bit, even dipping back down below 5%. What happens next with rates depends on where inflation goes from here.

The context: Three years ago, homebuyers faced similar borrowing costs and, at the time, rates were characterized as "historically low." And if we think borrowing money is expensive today, let's not forget the early 1980s when the Federal Reserve jacked up rates to never-before-seen levels due to hyperinflation. The average rate on a 30-year fixed-rate mortgage in 1981 topped 16%.

The upside: For homebuyers, a potential benefit to rising rates is downward pressure on home prices, which could cause the housing market to cool slightly. As the cost to borrow continues to increase with mortgages becoming more expensive, homes could experience fewer offers and prices would slow in pace. In fact, nearly one in five sellers dropped their asking price during late April through late May, according to Redfin.

On the flip side, less homebuyers mean more renters. Rent prices have skyrocketed, and housing activists are asking the White House to take action on what they call a "national emergency."

What about the stock market?

Dow Jones Industrial Average stock market index for the past 30 years

Macrotrends.net

Current conditions: Year-to-date, the Dow Jones Industrial Average -- a composite of 30 of the most well-known US stocks such as Apple, Microsoft and Coca-Cola -- is about 8.5% below where it started in January. Relative to the broader market, technology stocks are down much more. The Nasdaq is off almost 19% since the start of the year.

The benchmark S&P 500 stock index hit lows in June that marked a more than 20% drop from January, which brought us officially into a bear market. Since then, it's bounced back up a little, but some experts warn that a current bear market rally is at odds with expected earnings and we could see even lower stock prices in the near future.

The context: Stock price losses in 2022 are not nearly as swift and steep as what we saw in March 2020, when panic over the pandemic drove the DJIA down by 26% in roughly four trading days. The market reversed course the following month and began a bull run lasting more than two years, as the lockdown drove massive consumption of products and services tied to software, health care, food and natural gas.

Prior to that, in 2008 and 2009, a deep and pervasive crisis in housing and financial services sank the Dow by nearly 55% from its 2007 high. But by fall 2009, it was off to one of its longest winning streaks in financial history.

The upside: Given the cyclical nature of the stock market, now is not the time to jump ship.* "Times that are down, you at least want to hold and/or think about buying," said Adam Seessel, author of Where the Money Is. "Over the last 100 years, American stocks have been the surest way to grow wealthy slowly over time," he told me during a recent So Money podcast.

*One caveat: If you're closer to or living in retirement and your portfolio has taken a sizable hit, it may be worth talking to a professional and reviewing your selection of funds to ensure that you're not taking on too much risk. Target-date funds, a popular investment vehicle in many retirement accounts that auto-adjust for risk as you age, may be too risky for pre- or early retirees.

What does unemployment tell us?

US unemployment rates

Current conditions: The July jobs report shows the unemployment rate holding steady, slightly dropping to 3.5%. The Great Resignation of 2021, where millions of workers quit their jobs over burnout, as well as unsatisfactory wages and benefits, left employers scrambling to fill positions. However, that could be changing as economic challenges deepen: More job losses are likely on the horizon, and an increasing number of workers are concerned with job security.

The context: The rebound in theunemployment rate is an economic hallmark of the past two years. But the ongoing interest rate hike may weigh on corporate profits, leading to more layoffs and hiring freezes. For context, during the Great Recession, in a two-year span from late 2007 to 2009, the unemployment rate rose sharply from about 5% to 10%.

Today, the tech sector is one to watch. After benefiting from rapid growth led by consumer demand in the pandemic, companies like Google and Facebook may be in for a "correction." Layoffs.fyi, a website that tracks downsizing at tech startups, logged close to 37,000 layoffs in Q2, more than triple from the same period last year.

The upside: If you're worried about losing your job because your employer may be more vulnerable in a recession, document your wins so that when review season arrives, you're ready to walk your manager through your top-performing moments. Offer strategies for how to weather a potential slowdown. All the while, review your reserves to see how far you can stretch savings in case you're out of work. Keep in mind that in the previous recession, it took an average of eight to nine months for unemployed Americans to secure new jobs.

§

What's happening

Home prices overall are up by 37% since March 2020.

Why it matters

Surging home prices and higher interest rates make monthly mortgage payments less affordable.

What's next

Rising mortgage rates will make borrowing money more expensive, which will lessen competition to buy homes and eventually flatten prices.

Home prices continued to skyrocket in March as buyers tried to stay ahead of rising mortgage rates.

Prices increased by 20.6% this March compared to last year, according to the S&P CoreLogic Case-Shiller Indices, the leading measures of US home prices. This was the highest year-over-year increase in March for home prices in more than 35 years of data. Seven in 10 homes sold for more than their asking price, according to CoreLogic.

Out of the 20 cities tracked by the 20-city composite index, Tampa, Phoenix and Miami saw the highest year-over-year gains in March. Tampa saw the greatest increase, with an almost 35% increase in home prices year-over-year. All 20 cities experienced double-digit price growth for the year ending in March.

The strongest price growth was seen in the south and southeast, with both regions posting almost 30% gains in March. Seventeen of the 20 metro areas also saw acceleration in their annual gains since February.

"Those of us who have been anticipating a deceleration in the growth rate of US home prices will have to wait at least a month longer," said Craig Lazzara, managing director at S&P DJI, in the release. "The strength of the Composite indices suggests very broad strength in the housing market, which we continue to observe."

Since the start of the pandemic in March 2020, home prices overall are up by 37%. The current surge in home prices is a result of tight competition between buyers in a low-inventory market as they attempt to lock in lower mortgage rates before rates jump even higher throughout the year, as experts predict they will.

If you're considering buying a new home -- or are actively in the market -- the news isn't all bad. Interest rates are at their highest point in more than 40 years, and one potential benefit of that may, eventually, be downward pressure on home prices. As it becomes increasingly expensive to borrow money, fewer people will seek to do so, and homes for sale may receive fewer offers leading to, eventually, lower prices. In fact, nearly one in five sellers lowered their asking price during a four-week period in May and April, according to Redfin.

"Mortgages are becoming more expensive as the Federal Reserve has begun to ratchet up interest rates, suggesting that the macroeconomic environment may not support extraordinary home price growth for much longer," said Lazzara. "Although one can safely predict that price gains will begin to decelerate, the timing of the deceleration is a more difficult call."

Student loan interest rates inflation what is the impact of high inflation does high inflation cause recession does high inflation increase interest rates does high inflation help borrowers does high blood pressure make you tired does high blood pressure cause headaches does high humidity mean hot

Does High Inflation Impact Your Student Loans? For Most Borrowers, Yes

Does High Inflation Impact Your Student Loans? For Most Borrowers, Yes

This story is part of Recession Help Desk, CNET's coverage of how to make smart money moves in an uncertain economy.

Despite a slight slowdown in July, inflation remains sky high as prices continue climbing, making everything from the groceries you buy to the rent you pay each month more expensive. But how does inflation impact student loan borrowers?

The answer will vary depending on what type of loans you hold -- federal or private -- and whether or not you're eligible for loan forgiveness. In a general sense, however, inflation will make it harder for borrowers to repay existing debt and will continue to drive up rates on private student loans.

The current pause on federal student loan repayments expires at the end of August. The moratorium was extended six times since the start of the pandemic and has offered borrowers temporary relief. Yet when repayments begin, high prices can make it more difficult for borrowers to restart monthly student loan payments.

How exactly does inflation impact the student loan debt you hold? We sat down with student loans expert Mark Kantrowitz, author of How to Appeal for More College Financial Aid, to discuss the specifics of what inflation means for student loan holders.

The role inflation plays in student loans

The Federal Reserve has raised the federal funds rate four times in an effort to slow rampant inflation. But while prices haven't dropped from record-high levels, these hikes in the federal funds rate have indirectly led to more burdensome interest rates on consumer products, such as credit cards, mortgages and loans.

The Fed's rate increases won't impact any fixed-rate student loans you currently hold, for example, federal loans. But private loans with adjustable-rates (interest rates that can rise and fall along with the economy) may see their rates increase, making them more expensive for borrowers to repay.

If your wages were to rise alongside inflation at the same rate or higher, it could make paying back your debt a little bit easier and counter higher interest rates. "Inflation dictates that a dollar ten years ago is worth more than a dollar today. So, as long as your wages are rising along with inflation, the debt for a loan borrowed in the past will hold less value today," said Kantrowitz.

However, average wage increases are not keeping up with inflation. As of June, wages have only increased 5.1% over the past 12 months, making it more difficult for borrowers to chip away at their debt on top of covering daily expenses.

Here's a breakdown on how inflation might impact you depending on your loan type and whether or not you're still in school:

If you hold federal student loans:

Federal student loans are always fixed-rate loans, so the interest rate will stay the same over its lifetime.

If you hold a federal student loan, inflation could work in your favor because it effectively devalues your debt, but that only helps if your wages kept up or surpassed the inflation rate.

If, like for most Americans, your wages haven't increased substantially and your budget is stretched even thinner than before, this devalued debt won't help you -- and you might even find it more difficult to repay your loans when the federal loan repayment freeze ends.

If you hold private student loans:

Private student loans can be either variable or fixed rate, and payments for either type of private loan have not been on hold during the pandemic.

For those with fixed-rate private loans, the interest rate of your existing student debt won't go up. However, since inflation is making everyday purchases pricier, you might find yourself with less cash overall to set aside for paying off debt.

If you have adjustable-rate loans, your interest rates could definitely rise -- and may have already. As inflation rates go up, interest rates usually follow. Variable-rate private loans holders could see even higher interest rates in the future.

If you're a new borrower in 2022:

Both federal and private student loan interest rates will be higher for the 2022-23 academic year, Kantrowitz said. The new federal student loan interest rates for the 2022-23 school year are as follows:

Undergraduate loans: 4.99%

Graduate Direct Unsubsidized loans: 6.54%

PLUS loans: 7.54%

This is a big jump up for students. For reference, last year an undergraduate federal student loan had an interest rate of 3.73% -- around 1.25% lower than the rate for the coming academic year.

Private student loan rates have also increased. Fixed-rate private student loans range from 3.22% to 13.95%, and variable-rate private student loans range from 1.29% to 12.99%, according to Bankrate, which is owned by the same parent company as CNET.

Will inflation make loan repayment more difficult after the federal payment pause ends?

Kantrowitz said he predicts that the student loan repayment pause will be extended again, with renewed payments beginning after the 2022 midterms. Whether or not the student loan freeze is prolonged could hinge on the White House's decision on widespread federal student loan forgiveness. In any case, since the federal payment pause is set to expire in a couple weeks and no official announcements have been made, it's best to prepare for repayment now.

For many, repaying student loan debt in a time of high inflation is a real concern. According to the Student Debt Crisis Center, out of 23,532 borrowers, 92% of those who were fully employed are concerned about affording payments in the face of skyrocketing inflation.

"I personally have not been able to save for student loan repayment, and I don't think I could have given the growing disparity between wages and the national cost of living," said Jonathan Casson, a recent graduate of Cornell University.

If you're worried about repaying your student debt, here are some tips to plan ahead:

How can you prepare to repay federal loans?

1. Look into income-driven repayment plans

The government offers four income-driven repayment plans that can help make monthly payments more affordable for borrowers who need to keep payment sizes small. Each IDR plan caps payments at between 10% to 20% of your discretionary income (income after taxes and necessities are paid), and forgives your loan balance after 20 or 25 years of payment. Eligibility for these plans is dependent upon family size and discretionary income.

2. Check if you're eligible for loan forgiveness

If you're a teacher, first responder, public servant or government worker, you may be eligible for federal student loan forgiveness under the Public Service Loan Forgiveness program. You must be in a qualifying position, hold eligible federal student loans and have made 120 qualifying payments to receive forgiveness (each paused month during the federal payment freeze counts as one qualifying payment).

The PSLF has temporarily expanded its benefits to include forgiveness for more federal loan types and IDR plans, and could make some applicants now eligible who had been denied loan cancellation in the past. The expanded forgiveness waiver application is due by Oct. 31, so it's important to find out if you're eligible now. In some cases, you may need to consolidate your loans into federal Direct Loans, a process that can take 45 days.

While your monthly payment may not change if you haven't reached the 120 payment goal yet, you'll at least be a step closer toward student loan forgiveness.

3. Refinance private loans

With many interest rate hikes expected this year, refinancing your private adjustable-rate student loans into fixed-rate student loans could help you save hundreds to thousands in interest -- and may even reduce your monthly payment. You should only refinance if you receive better payment terms or a lower rate. Otherwise it generally won't be worth the hassle and could cost you more in interest.

4. Review your budget

If a student loan payment is not feasible with your current budget, see if there are any ways to cut expenses or pay down high-interest debt now to free up funds. While adjusting your budget may seem daunting, there are multiple resources and apps to help you calculate and identify expenses you can reduce or eliminate.

5. Consider a side hustle

A part-time gig outside of your primary job may help supplement your income as inflation skyrockets. Currently, 31% of American adults have a side hustle, according to a 2022 Bankrate survey. Having an additional source of money can help bridge a gap in your budget and offer you a bit of breathing room.

Best ev charger for 2022 jeep best ev charger for nissan leaf best ev charger for chevy bolt best ev charger for tesla best ev charger for bolt best ev charger for mach e best ev charger consumer reports best ev charger for nissan leaf best ev charger for tesla model 3 best ev cars 2022 best ev vehicles

Best EV Charger for 2022

Best EV Charger for 2022

If you're taking the plunge and buying your first electric car, pickup or SUV, you'll also want to buy and install a Level 2 home charger.

There are things to think about when you pick a Level 2 EV charger, but the value in one is straightforward. For the vast majority of drivers, Level 2 will limit and probably eliminate reliance on a public charging station, and it will remove the anxiety that goes with finding an unoccupied public charger when you need it. Just about any Level 2 charger should fully charge your electric vehicle's battery overnight, even if the battery is nearly depleted.

A Level 2, 240-volt home charger will charge your electric car much much faster than the Level 1 charger that comes with the vehicle. There are more Level 2 chargers to choose from each month, and they might be less expensive than you'd guess. Set up and installation don't have to be complicated or expensive, either, depending on your circumstances. Many Level 2 EV chargers can be plugged into an outlet just like the Level 1, which comes with your car. Others can be hard-wired into household electrical if that's the better option for your purposes. Many have their own phone apps to manage charging and minimize cost.

This list aims to give you some foundation for choosing a home EV charger. I've studied a broad range of chargers across the price spectrum and based my recommendations on expert interviews, user feedback, personal experience and the work of testing labs such as Consumer Reports and Underwriters Laboratories. Browse the full list before you click through, then follow on for a primer on just about everything you need to know when choosing an electric vehicle charger.

Enel X

The JuiceBox 40 delivers everything you need and most of what you'll want in a Level 2 home charge station, at a reasonable price. It's UL listed, built to exceed NEMA 4 standards and great for outdoor use. It can be hardwired or plugged in. It will charge any electric car, pick-up or SUV available in North America, including Tesla with the brand's standard J1772 adaptor, and it comes with the industry standard three-year warranty. Perhaps most important, it hits the magic charge-rate threshold of 40 amps, which means it will replenish any substantially drained EV (current or forthcoming) in an 8- to 10-hour time frame for years to come.

Beyond its foundational features, the JuiceBox 40 is finished with some polished and useful details. It's easy to install, and it's 25-foot connector cable allows maximum flexibility in use. Even its plug-in cord is longer than most, and that adds flexibility when mounting the box in relation to the necessary 240-volt plug. JuiceBox 40 has a built-in cable rack and security lock and, according to experts, one of the best control apps going. It can be started with voice commands through Amazon Alexa or Google Home, and you can use the app to set reminders, program charge hours and monitor energy consumption (and cost) precisely.

ChargePoint

ChargePoint started in the EV business building public charge stations. The Home Flex represents its expansion into residential, Level 2 chargers.

Home Flex has nearly everything you'll find in our Best Overall JuiceBox 40, with even a bit more to like. Its box is compact and stylish, and its connector locks into its holster or a charge port with a smooth, authoritative click. The holster is ringed with a softly glowing halo of an LED. More significantly, Home Flex can raise the peak charging rate to 50 amps if it's hardwired. While that's almost overkill in a Level 2 charger, given that 40 amps should still charge any EV overnight for years to come, Home Flex will charge a few more current EVs (a couple Teslas and the Ford Mustang Mach E) at their fastest possible rate on residential Alternating Current.

Wired for 50 amps, Home Flex is likely to add some installation cost. Its connector cable is a couple feet shorter than JuiceBox 40's, and its box-to-outlet cord is shorter, too. Those things can matter, but they're not what relegate Home Flex to runner-up status, in our estimation. It's just simple, rational arithmetic. ChargePoint's Home Flex costs at least $100 more than JuiceBox 40, and that cash would make a significant contribution to whatever installation costs there might be.

United Chargers

The Grizzl-E Classic car charging station is designed and built in Canada, and that could be one of the reasons we like it. The Classic ships as a plug-in, to minimize potential installation costs, but it's also suitable for hardwiring. It's manually adjustable from 16 to 40 amps, and that can save on installation, too, in the short run (as in you might not need a higher-rated, more expensive circuit breaker until you have a car that needs the higher charge rate).

Throw in a 24-foot connector cord, and that's about it. There's no Bluetooth connection or phone app here. Yet calling the Grizzl-E Classic a no-frills, charge-your-EV-fast Level 2 undervalues one of its other strengths. This thing is built like a tank, and packaged in a dustproof, fire-resistant aluminum case that's built to NEMA 6 standards, which protect against full water immersion to one meter for 30 minutes. Most other home stations are "upgraded" at NEMA 4.

This is a great charger for folks who like it simple. The Classic is well built, well warrantied (three years) and often cited for good customer service. You'll look a long time trying to find another home station with 40 amps of charging and this kind of quality at this price.

United Chargers

The Grizzl-E Duo is a carbon copy of our Best Value Grizzl-E Classic. Or maybe that's a double copy, because the Duo adds a second 24-foot cable and connector to charge two cars simultaneously.

Beyond that, it's basically that same no-frills, rugged, high-output charge station, though there is another feature unique to the Duo. It adds an intelligent power-sharing circuit to maximize available current between the two charging cars according to each car's need, up to 40 amps total. That in turn maximizes charge speed for each vehicle, without risk of blowing a circuit.

Wallbox

The Pulsar Plus is an extra-compact Level 2 residential charge station. It's suitable for outdoor use, with 40 amps of charging power and most of the preferred features, including a 25-foot connector cable and a mobile app. And if the app loses its connection with the charger, or you don't feel like messing with it, you can just plug in your EV and charge.

Yet what separates Pulsar Plus from nearly all other home charge stations is its Power Sharing feature. This allows more than one unit to be connected to the same electrical circuit to safely charge multiple EVs at once without exceeding the circuit's capacity. Built-in smart power management automatically balances charging to ensure the most efficient energy distribution among the various chargers on the circuit, no need for extra hardware. Further, Wallbox says it's developing the capability to meter each Pulsar Plus charger separately and directly bill individuals. This might be your future if home is a multi-unit dwelling shared with other occupants.

ClipperCreek

ClipperCreek began building home and commercial chargers at its factory in Auburn, California, in 2009, and its HCS-40 Level 2 home station is one of the best-selling chargers to date. In 2022, the box that houses the hardware is larger than most competitors, and the HCS-40's charge rate maxes out at 32 amps. That will still charge most electric vehicles on the road today at their highest rate possible on household current, but it's about 20% less than experts recommend for the long view.

Beyond that, the HCS-40's features still hold up well. Its case is rated NEMA 4 for extreme weather, and its connector cord measures 25 feet. It comes with a remote connector holster that you can hang where you want it -- as in right next to your EV's charge port, wherever that may be. It has a keyed lock that can secure the connector in your charge port or the holster, and there's even an optional cord retractor. It's warranted for three years, and ClipperCreek's customer service is praised in EV circles.

Siemens

Siemens has been making industrial electrical equipment, automotive components and imaging devices for 170 years, and it was an early adaptor to home EV chargers, too. When it was introduced in 2016, the US2 VersiCharge was consistently rated one of the best Level 2 home charge stations available.

Today, the VersiCharge console or case is bigger than just about any out there, and its connector cord is hardly the longest (20 feet). With a peak charge rate of 30 amps, it will still max charge most EVs on the market, but it doesn't leave much growth for the future.

Still it's prized by many EV owners. That's partly for its charm and partly for its build quality. US2 VersiCharge meets NEMA 4 standards for rough weather, with a rugged metal case that looks like the adornment on a big Art Deco building. It even offers its own bespoke outdoor post. It has a couple of buttons that let you delay the start of charging when you plug it in up to 8 hours, and it's known for reliability. It's also warranted for three years, which remains the industry max.

Dcbel Energy

Designed and built by Montreal-based Dcbel Energy, the R16 is much more than a Level 2 home charge station. Think of it as the electrical command center for the home of the future, with its own operating system.

The R16 allows solar-collected Direct Current to charge your EV or home batteries, and DC is by far the fastest way to charge your car. It will turn solar DC into Alternating Current to power your home, and it can turn your EV into a household power bank in the event of utility failure. The R16 can integrate and replace up to five pieces of hardware early solar and low-carbon adopters now use in their homes.

It will work like a conventional Level 2 home charge station on AC, in case you're still in the process of building your solar array. It has two connector cables to charge two electric cars, pickups or SUVs at once. Foremost, the R16 represents the next big thing in EV charging. It's one of the first chargers to market that allows bi-directional charging, which can turn your electric vehicle--or at least some electric vehicles, like the new Ford F-150 Lightning -- into backup power for you home when it's sitting in the driveway. Depending on the size of your car's battery, that could power your home at full bore for at least a day or two, or on emergency rations for 10 days or more. For more on bi-directional charging, read on to EVSE 101.

MeGear

The MeGear Level 1+2 Charger looks a lot like the manufacturer-issued Level 1 charge cord that comes with the typical electric vehicle. It's 25 feet long and has an adapter that allows you to plug it into a typical, three-prong, 120-volt household outlet. If you do that, the MeGear Level 1+2 will charge your EV at essentially the same rate as the cable that came with the car. But if you happen to have access to a 240-volt outlet with a NEMA 6-20 plug (a lot of electric clothes dryers use these), MeGear Level 1+2 will raise your charge rate to 240-volt Level 2. A device like this one is the cheapest path to Level 2 charging.

Now, we've seen this charger marketed under a few different brand names. While the other chargers on our Best list all come with a three-year warranty, the MeGear Level 1+2 is warranted for only a year. It's also the only one that won't restart itself after a power interruption, even if that interruption is only momentary. You'll have to restart it yourself, so hopefully the interruption doesn't occur just after you turn in for the night.

Like we said: this is the cheapest path to Level 2 charging. Quite a bit cheaper, even, than buying a replacement Level 1 cord from your EV dealer. The MeGear Level 1+2 charges on 240 at the lowest Level 2 rate of 16 amps -- much lower than the optimal, future-protecting 40 or 50 amps. Yet at 16 amps, Level 2 should charge your EV about three times faster than the Level 1 cord that came with it. With this charger you can continue to save your pennies for a more powerful Level 2 home station. In the meantime, you'll be able to take advantage of Level 2 when you can and worry less about making it to work the next morning if you can't find a public charger on the way home.

Comparison of the best EV chargers for 2022

Charger

Level 1 or 2

Max charge rate

Connector cable length

Hardwired or plug-in

Phone app

Features

Best EV charger overall

Enel X JuiceBox 40 Smart Electric Vehicle Charging Station

2

40 amps

25 feet

Both

Yes

Everything you need for fast, easy home charging, and most of what you'll want. The right features at a good price.

Best EV charger overall runner-up

ChargePoint Home Flex Electric Vehicle Charger

2

50 amps (hardwired)

23 feet

Both

Yes

A bit slicker than best overall, and it can raise max charge rate to 50 amps (assuming your car could take that charge rate). But it also costs more, and fitted for 50 amps, could cost more to install.

Best EV charger value, especially if it's going outdoors

United Chargers Grizzl-E Classic EV Charging Station

2

40 amps

24 feet

Both

No

A simple, rugged home station that charges EVs fast. Comes with the highest weather protection standard.

Best EV charger for charging two cars

United Chargers Grizzl-E Duo Plug In EV Charger

2

40 amps

24 feet

Both

No

Two connectors, and internal controls that automatically balance power for maximum efficiency and charge speed.

Best EV charger if you need two or more ganged

Wallbox Pulsar Plus Electric Vehicle Smart Charger

2

40 amps

25 feet

Both

Yes

Safely allows multiple chargers on a single electrical circuit. According to the manufacturer, it'll soon add separate metering (and billing) for each one.

Best EV charger from the start of the new EV age

ClipperCreek HCS-40/HCS-40P Charging Station

2

32 amps

25 feet

Both

No

An all-time top seller, from an early adapter known for customer service.

Best EV charger from an old-school brand

Siemens US2 VersiCharge Universal EV Charger

2

30 amps

20 feet

Both

No

Built like a tank, looks like Art Deco, from one of the world's oldest electrical suppliers. Still charges most electric cars at the maximum possible rate on household current.

Best home EV charger if money is no object

Dcbel R16 Home Energy Station

2+

DC charging capable (with solar)

Up to 20 feet

Hardwired

Yes

More like a home electricity substation, managing solar, batteries, charging and household supply with its own OS. As a Level 2 EV charger, it's one of the first to enable bi-directional charging, which can turn your EV battery into a power bank for your home.

Best EV charger for cheapskates, bi-voltage edition

MeGear Level 1+2 Home Electric Vehicle Charging Station

1 or 2

16 amps at 240 volts

25 feet

Plug-in

No

About the least expensive path to Level 2 charging, and it will work as a Level 1 until you have access to 240-volt AC. Much slower than more powerful level 2s, but still about three times faster than the Level 1 that comes with your car.

Wallbox

EVSE 101

The thing you use to plug in an electric car, pickup or SUV is not, technically, a charger. The charging hardware and control system are actually inside the vehicle's powertrain. The plug-in thing is Electric Vehicle Supply Equipment, and it allows the transfer of energy between an electric utility and the EV. This equipment includes charge cords, charge stands (residential or public), attachment plugs, vehicle connectors and bits of electrical hardware that ensure safe operation for user and vehicle. But don't worry. You can call your EVSE a charger.

Every electric car should come with a charger -- invariably a heavy cord with a large, block-shaped device between the vehicle connector and the wall plug. If you bought your electric vehicle used and it didn't come with its charge cord, I hope you accounted for that in the transaction price.

These cords are called Level 1 chargers, and they plug into a standard 120-volt electric outlet on your house or in your garage. They're fine for plug-in hybrid vehicles, which typically have fairly small batteries and a gasoline engine to power the car, and a Level 1 cord will charge a full electric, no-engine car. It won't charge a pure EV anything close to quickly. If your daily electric-car rounds amount to 20 or 25 miles, you can probably live with Level 1. But if you happen to pull your electric car into the driveway with its battery nearly depleted, it can take literally days with a Level 1 charger to replenish to full capacity.

Dcbel Energy

I wouldn't recommend buying another Level 1 charger, unless you need to replace the one that came with your EV or want a second for an alternate location. No Level 1 charger -- from the vehicle manufacturer or an aftermarket supplier -- will charge your EV substantially faster than the cord that came with it. The money you'd spend on a Level 1 charger will get you a long way toward something called a Level 2 charge station, and you can still take the Level 1 cord that came with your car wherever you go. If you want maximum convenience and don't want to rely on public, high-speed charging stations, you probably want Level 2. If your daily rounds regularly use 100 miles of range or more, you absolutely want Level 2. I'll elaborate shortly.

First, I'll answer a question many EV shoppers are likely to have. Every electric car, truck and SUV sold in North America comes with the same connector in its charge port. Every car that's not a Tesla, that is. This standard connection is called SAE J1772, and it means that you don't need to worry about buying the wrong EVSE. Every charge cord and station, home or public, will plug into every electric car, truck or SUV on the road -- including Teslas. That's because every Tesla vehicle comes with an adaptor that allows a J1772 plug to fit in its proprietary charge port. And as Tesla ponders rolling out its private, national Supercharger charging network to non-Tesla owners, it's developed an adaptor that allows its proprietary connection to fit into the J1772 port on other manufacturers' electric vehicles.

Take it up a level

Level 2 EV chargers are a major upgrade from the Level 1 device that comes with an electric car. While it won't charge as quickly as a public DC charger, Level 2 is the best most of us will get for home charging -- or at least those of us who aren't certified millionaires or better. There are 480-volt fast chargers that can theoretically be installed for residential use, but they're expensive to begin with and have specific power requirements, including a dedicated power line. In short, the cost of a 480-volt charge station is prohibitive for the typical homeowner.

ChargePoint

How big is the Level 2 upgrade? A Level 1 charger delivers about 12 amps, give or take a couple, and adds three to five miles of range to a typical electric car in an hour. A Level 2 charger delivers a minimum 16 amps and as many as 80, with a rate of 12 to 60 miles of range per hour of charge, depending on the car and the specific charger. Bottom line, a Level 2 charger can charge an EV three to 10 times faster than a Level 1 charger can, and you can buy good, higher-amperage Level 2 charging stations for $500 all day.

Level 2 chargers require 240-volt electrical supply. If you're not up to speed on electrical current, you shouldn't let that requirement put you off. While there may be some preparation or installation costs, drawing 240 volts from typical residential electrical is not a major or particularly expensive proposition. Many homes already have 240. Yours may, too, if you have an electric water heater or clothes dryer, and if you do there's a good chance it's already in the garage, where you'll need it for a Level 2 charge station.

If you live near a major population center and don't drive a lot, you may not need a Level 2 EV charger. If you live in a rural area with less developed infrastructure, you probably do need one. Wherever you live, the more and further you drive your electric car, pickup or SUV, the more valuable a Level 2 charger will be. Level 2 can substantially reduce the small hassles and anxiety of owning an electric car. For upwards of 90% of the driving public, it can eliminate reliance on public charging stations, unless or until you take your electric car on a long-distance driving vacation.

ChargePoint/Dcbel/United Chargers/Wallbox

Getting ready

There are a handful of things to think about before installing a Level 2 charger, but the first comes down to where you live and who controls your electrical supply.

If you own a home, that's probably all you need to know. You're the boss, and you can proceed with a Level 2 charging station. If you own a condominium, you'll likely need permission from the owner's association. That could be as simple as filling out a form, or it could require jumping through a few more hoops, but you should start by reaching out to the association or property management company. If you rent a home or live in an apartment with reserved parking or a garage, hope is not lost. You'll still have to get the landlord's permission, then determine how much power is available in the parking area and how it's metered.

If you don't have 240-volt current, that's not a huge challenge. The first thing you need is an electrician to tell you whether your existing electrical panel has sufficient capacity for a 240-volt line. There's a reasonable chance it does, but if it doesn't, you'll have to upgrade. And even if you have existing 240-volt service, it's best to consult an electrician as you prepare for a Level 2 charging station.

Let's say, for example, that you already have an electric dryer, and it's in the garage not far from where you want your Level 2 charger. There's a good chance you can find a Level 2 charger that will plug into the same outlet as the dryer (most plug-in Level 2s offer one or two of three common 240 plugs -- NEMA 6-20, 6-50 or 14-50, with NEMA standing for the National Electrical Manufacturers Association). This path means you'll never be able to charge your car and run the dryer at the same time, however, so a good electrician seems like a good place to start. Different surveys by different organizations put the average cost of installing a Level 2 charge station between $650 and $800. That's on top of the charger, of course.

Wallbox

While you're waiting for the electrician, think about where you want the charge station to go. That's typically on a wall inside or outside the garage, or on a post near where you park. Outside is no problem, but you should know it's going outside before you pick your charger, and you should also know where the charge port is located on your electric car, truck or SUV. No two electric vehicle makes put their charge ports in exactly the same place, and the cords on Level 2 charge stations typically range from 12 to 25 feet.

Lastly, check what's available in your locale when it comes to rebates, tax credits and other incentives for installing an EV charge station. The IRS offers a tax credit equal to 30% of the cost, up to $1,000. Your state and local government may offer incentives as well, and don't forget to check your electrical utility.

Big things to think about

Home chargers for electric cars are proliferating, and there are more to choose from all the time. Nearly every vehicle manufacture offers its own, branded charge station through its sales points, typically with third-party installation. If convenience is more important than cash outlay, or if you're a committed brand geek, you can certainly go with the manufacturer's product. On the other hand, you'll do at least as well on quality and performance for less money if you choose your own Level 2 charger. Often substantially less money.

Question 2 when choosing a Level 2 home charger for your electric car, pickup or SUV: Do you want one that's hardwired or one that plugs into an outlet, like the Level 1 charger that comes with the car? Hardwiring means the station is semi-permanently connected to your home's electrical grid, and you won't be able to move it without opening a junction box and detaching the wiring. A plug-in station simply plugs into a 240-volt electrical outlet. Think of it like a permanently installed light fixture versus a plug-in lamp. Other things being equal, a plug-in charge station will work as well as one that's hardwired. The primary advantage of the plug-in is that you can more easily remove it and bring it with you -- if you relocate, for example.

Dcbel Energy

Other things are rarely equal, though, and there are a few more subtle things to consider when choosing between hardwired and plug-in. Most local electrical code will require a charge station installed outdoors to be hardwired. Plug-in charge stations are limited to 40-amp output, and while 40 amps of charging power is more than adequate for the foreseeable future (I'll get to that next), the ultimate future-proof charging station might have a higher charge rate. A plug-in charger won't eliminate additional installation cost, either, unless you happen to have an appropriate 240-volt plug in your garage, in close proximity to where you want the charge station. If that's the case, we'd definitely recommend a plug-in Level 2.

Most Level II chargers are packaged in a case designed to be mounted to a wall or post. Removal and relocation require that they be detached, which can be as simple as removing a couple of fasteners. Yet there are an increasing number of more portable Level 2 chargers, as well as bi-voltage chargers that work at Level 1 or Level 2 depending on the receptacle they're plugged into. These look similar to the Level 1 charger that comes with the car -- usually a long, heavy cord with a plastic brick somewhere between the outlet plug and the vehicle connector. Portables can be useful for travel or commuting because they'll work at Level 2 in the event you have access to a 240-volt plug at work or a vacation residence. The drawback is simple, however. Portable bi-voltage chargers often max out at 16 amps output, or occasionally 20 amps, and while that's better than anything Level 1 can deliver, it won't bring the potential charge speed of higher-amperage Level 2 home stations .

With Level 2 charge stations, output amperage is king. Sort of. Level 2 delivers at least 16 amps and as many as 80, and the chargers tend to get more expensive as output amperage increases. Accounting for one important limitation, the charger with the highest output amperage will charge your electric car fastest. Yet that limitation is big, and it's the reason you need to know the maximum charge rate your electric car, pickup or SUV will accept.

Siemens

You'll find your electric vehicle's maximum charge rate in its owner's manual, on the spec sheet or in the worst case from the manufacturer. It may be listed in kilowatts, or kW, and if that's the case you should Google a kilowatts-to-amperes conversion calculator and convert the kW at 240 volts. This isn't a safety issue: A charger with a higher charge rate won't somehow melt your electric car. But your car's maximum charge rate matters when you decide how much to spend on a Level 2 charger, and which one to choose. If its max charge rate is 16 amps, it's never going to charge faster than 16 amps on household current, no matter how many amps your Level 2 charger can deliver. Find one of those expensive 80-amp chargers, which will very likely require some serious infrastructure improvements to your household electrical, and your car is still not going to accept a charge rate greater than 16 amps.

Does that mean you should never buy a charger that delivers more amps than your electric car, pickup or SUV can accept? It definitely does not mean that, unless you consider the charger a short-term investment to ditch when you get your next car. A short history of the current crop of electric cars explains why choosing a Level 2 charger based strictly on your current car's max charge rate might not be the best idea.

When it was introduced in 2011, the Nissan Leaf could accept a maximum charge of about 14 amps on household current, adding five or six miles of range per hour of charging. With updates for model year 2016, the Leaf could charge at 28 amps. Around 2018, the Chevy Bolt, Jaguar I-Pace and Kia Niro EVs debuted with a max charge rate of about 30 amps, good for 23 to 24 miles of range per hour. Ford's recently introduced Mustang Mach E, and some Tesla models, can charge at 48 amps on AC, adding 35 miles of range per hour of charge. And charge rates for electric cars are likely to increase further over the next several years as new models roll out.

If the point isn't clear, we'll put it another way. Your first electric car may charge at a max of 16 amps, but it's very likely that your next one, brand new or used, will take a charge at a faster rate. Given the outlay for a Level 2 charge station, you probably want to protect your investment. You might save a few bucks now with a low power Level 2, but there's a good chance you're going to want a more powerful one when you get your next electric car.

Megear

If you're now wondering by exactly how much you should future-proof your Level 2 charge station, we have a simple rule of thumb. Experts generally agree that a home charger output of 40 amps -- or 50 amps at the extreme -- will be sufficient for the typical electric car owner for years to come.

"Forty amps seems to be the sweet spot," says Barry Woods, the director of vehicle innovation at ReVision Energy in Maine, and a board member for the trade group Plug In America. "A 40-amp charger is sized correctly for most residential locations, and 40 amps is going to be relevant for a while. That's based on driving habits more than technology. Given the batteries we have now, and what we anticipate, 40 amps should adequately meet the needs of the vast majority of users."

A 40-amp Level 2 charger should cover the daily range requirements of more than 95% of drivers in the United States, including those in rural areas, based on reams of data collected over decades. Your next electric car could charge at a rate faster than 40 amps, but 40 amps will still replenish its deeply depleted batteries in an 8-to-10-hour time frame. Ten hours at 40 amps will add roughly 300 miles of range, depending on the vehicle.

You could consider a 50-amp charger, to take advantage of the higher household charge rate in a few current electric vehicles, but the charger will cost more than a 40-amp max charger. The 50-amp demands heavier-gauge wiring, a higher-rated circuit breaker and a higher-capacity electric panel, so there's a good chance it will cost more to install, and its advantage for household use is minimal -- maybe just bragging rights. A Level 2 charger rated at more than 40 amps will have to be hardwired, so it eliminates the option of a plug-in charge station that you can take with you when you move.

ClipperCreek

In 2022, a 40-amp Level 2 charge station almost certainly delivers the best cost/benefit breakdown for your electric car, pickup or SUV, and it should deliver sufficient charge speed for years to come. And remember. Even if your current electric vehicle charges at a maximum rate less than 40 amps (most do), there's nothing to worry about. The electric car controls how much electricity its battery absorbs when it's charged, so you can't damage the vehicle with a charger capable of a higher rate.

More things to look for

If the charge amperage thing gets confusing, think of 40 amps as the target and work up or down from there, based on cost, features and preferences. The next thing to think about when choosing a Level 2 charger is the weather -- or specifically, whether your electric car, pickup or SUV is going to sit out in the weather. If you can't or won't park your electric car in a covered garage, the charge station probably needs to go outdoors, too. In that case, to be in code, it will need to be hardwired and not plugged in. It will also need to be rated for outdoor use.

Most Level 2 chargers, including those on our Best list, are rated at least NEMA 3, and NEMA 3 is acceptable for outdoor use. Some chargers are built to NEMA 4 standards, which add another layer of protection and shield the box against direct pressure from a garden hose. If there's lots of rain where you live, and it's often driven by stiff winds, NEMA 4 is a good choice. Whether your Level 2 charger is going in the garage or out, it's always smart to choose one listed by Underwriters Laboratories or Edison Testing Labs. The UL or ETL listing designates compliance with safety standards established by these nationally recognized testing labs.

Next are the physical features of the charger itself, starting with the connector cord. Level 2 charge cords typically range from 12 to 25 feet, and longer is almost always better. A 12-foot cord can cut it close in the best of circumstances, and might require that you park your car in the same direction or orientation every time you plug it in. The 25-foot one should allow you to park in at least two different spots if your garage has two bays or more. It should cover things if you the charge port on your next electric car is in an entirely different spot than your current car's.

ChargePoint

Many chargers come with a horn to hold the looped cable. Others expect you to wrap the cable around the box, or a long nail of your choosing, or to simply leave the cable coiled on the ground or floor. Pay attention to these details if you're not fond of clutter, trip hazards or excessive dust accumulation. Look for a charger that has a holster for its connector, or at least a cap to cover the connector when it's not in use. Finally, consider the dimensions of the charger box itself. A really wide one might not fit the space between two single garage doors. A thick one that sticks out relatively far might make it more difficult to squeeze between the car and a wall in a tight, single-car garage.

Some early electric car chargers would not restart themselves if the power temporarily failed and then came back. You had to unplug the connector, then plug it back in to restart. Most current Level 2 chargers, including those on our Best list, will restart automatically, but make sure that's the case when you choose. It's better than waking up to find your electric car is not sufficiently charged.

Beyond that automatic restart feature, some chargers have just a few LEDs to tell you what they're doing. Others have a few hard buttons to set features or manually delay starting the charge once the vehicle is plugged in. Still others come with a phone or tablet app that connects to the charger via Wi-Fi or Bluetooth and shares a range of data and control options.