Step into a world where the focus is keenly set on what a year it. Within the confines of this article, a tapestry of references to what a year it awaits your exploration. If your pursuit involves unraveling the depths of what a year it, you've arrived at the perfect destination.

Our narrative unfolds with a wealth of insights surrounding what a year it. This is not just a standard article; it's a curated journey into the facets and intricacies of what a year it. Whether you're thirsting for comprehensive knowledge or just a glimpse into the universe of what a year it, this promises to be an enriching experience.

The spotlight is firmly on what a year it, and as you navigate through the text on these digital pages, you'll discover an extensive array of information centered around what a year it. This is more than mere information; it's an invitation to immerse yourself in the enthralling world of what a year it.

So, if you're eager to satisfy your curiosity about what a year it, your journey commences here. Let's embark together on a captivating odyssey through the myriad dimensions of what a year it.

20 year interest rates for september 2022 blank 20 year interest rate for mortgage 20 year interest rates mortgage current 20 year interest rates 20 year interest rate history halloween h20 20 years later 20 year anniversary gift 20 year mortgage rates 20 year anniversary symbol

20-Year Interest Rates for September 2022

20-Year Interest Rates for September 2022

Although a 20-year fixed-rate mortgage is a less common choice for a home loan than a 15- or 30-year mortgage, it has some advantages to consider when buying a house. A 20-year mortgage is a home loan you take out that you repay over a 20-year period. It also has a fixed interest rate just like 15- and 30-year mortgages do.

In a rising interest rate environment, a 20-year mortgage has some benefits over a 30-year mortgage. Since it's a shorter loan term you will end up paying a full decade less in interest, which adds up to tens of thousands of dollars in savings.

Here's everything you need to know about what a 20-year mortgage is, how they work and how to find the lowest mortgage rates possible.

What is a 20-year mortgage?

A 20-year mortgage works the same way as 15- and 30-year mortgages, it just has a 20-year term instead. You'll still need to meet all the same criteria and qualify with a lender or bank to be approved for this home loan type.

Comparing a 20-year and 30-year fixed rate mortgage

How does a 20-year home loan stack up to a 30-year mortgage? A 20-year term has the benefit of simply being paid off in a shorter amount of time. You'll have a higher monthly payment for two decades, but save yourself 10 years of interest on your loan.

Comparing a 20-year and 15-year fixed rate mortgage

While similar to a 15-year mortgage, with a 20-year mortgage, you'll have lower monthly payments, but pay five additional years in interest. What length mortgage you choose will depend in part on how high of a payment you can afford. A 20-year mortgage may be a good compromise if you can't afford the monthly payment for a 15-year mortgage, but don't want to stretch your loan terms out to 30 years.

No matter what term length you choose for a mortgage, it's important to do your research and interview numerous lenders before committing to one. This will help you find the lowest rate and fees available for your personal financial situation. The more lenders you talk to, the greater your chances of finding a lower rate. Even half a percentage point can make a big difference in the amount of interest you pay over the life of your mortgage.

20-year fixed mortgage trends

Right now, 20-year fixed-rate mortgage rates are hovering in the mid to upper 5% range, according to Bankrate, which is owned by the same parent company as CNET. Mortgage rates were at their highest levels in 14 years earlier this year, and have been consistently climbing since January when rates were still historically low and closer to 3%.

Depending on what happens with inflation, mortgage rates may remain relatively flat or they could keep increasing. The Federal Reserve is likely to continue raising rates over the course of the year, as economic conditions like inflation continuing to put additional pressure on rates. If you're considering buying a home, it's likely that mortgage rates are currently lower than they will be by the end of 2022. This means it could make sense to buy a home now, rather than waiting.

You can use CNET's mortgage calculator to figure out how much a difference in interest rates will cost you for your mortgage.

Current mortgage and refinance rates

We use information collected by Bankrate to track daily mortgage rate trends. The above table summarizes the average rates offered by lenders across the country.

Pros of a 20-year fixed-rate mortgage

Here are some key benefits a 20-year home loan offers over standard 30-year fixed-rate mortgages:

Save money on interest: You will save thousands of dollars in interest over the life of your loan compared to a 30-year mortgage.

Pay off loan faster: You will pay off your mortgage 10 years earlier than the most common type of mortgage, which is a 30-year fixed-rate mortgage, as well as building up equity in your home faster.

Cons of a 20-year fixed-rate mortgage

And here are some reasons why a 20-year mortgage may not make as much sense as a 30-year home loan.

Higher monthly payments: You have to be able to afford the monthly payments on a 20-year mortgage, which will be higher than a 30-year mortgage and may eat into your monthly budget.

How do you qualify for a 20-year fixed-rate mortgage?

You apply for a 20-year mortgage the same way you do for other types of mortgages. You must qualify with a lender or bank who is willing to lend you the money. The lender will take into account almost every aspect of your financial life to determine whether or not you can pay back the loan -- you'll submit financial documents like tax returns and pay stubs to apply for a home loan.

Information like your credit score, your income, how much debt you're carrying and your loan-to-value ratio all affect the rate a lender will offer you.

Other mortgage tools and resources

You can use CNET's mortgage calculator to help you determine how much house you can afford. CNET's mortgage calculator takes into account things like your monthly income, expenses and debt payments to give you an idea of what you can manage financially. Your mortgage rate will depend in part on those income factors, as well as your credit score and the ZIP code where you're looking to buy a house.

Playstation plus review a great deal that s also a real mess cartoon playstation plus review a great deal that s also a real me playstation plus review a great deal that spells playstation plus review a great deal that s a feeling playstation plus review anime playstation plus membership review playstation plus free games playstation plus deals

PlayStation Plus Review: A Great Deal That's Also a Real Mess

PlayStation Plus Review: A Great Deal That's Also a Real Mess

Sony's PlayStation Plus subscription game service, originally intended to sell online gaming access, went through a big change in June. Still called PS Plus, it has now become Sony's version of Xbox Game Pass, offering access to a large and evolving Netflix-style catalog of games. While it does some things better than Microsoft, the new PS Plus still lags behind in other aspects of the service.

The new PS Plus offers three subscription tiers, from an Essential package that mimics the old PS Plus, to Extra and Premium tiers offering hundreds of games, cloud streaming, monthly bonus games and online multiplayer access. What it doesn't offer, however, is a clean interface to make it easy to find games, and it also includes only a few of the biggest Sony games on the PlayStation platform. PS Plus mostly lines up with Xbox Game Pass on paper when you're going down a list of features. But for overall value and accessibility, it doesn't always feel like that when actually using it.

PS Plus is a big plus

Before the big update, Sony offered two different PlayStation subscriptions. PS Plus for playing online, with a couple of bonus games every month, was $10. PS Now offered a catalog of mostly older games to download or cloud stream for the same price. The new PS Plus combines the two under a single name and comes in three tiers:

Essential: Same as the original PS Plus, with two or three bonus monthly games, which you keep only as long as you're an active subscriber; online play; cloud saves; and PSN Store discounts. It costs $10 a month, or $60 a year. (In the UK it's £7 a month or £70 a year, and in Australia it's AU$12 or AU$80.)

Extra:All the features of Essential and more than 400 PS and PS5 games available to download or selectively stream. It costs $15 a month, or $100 a year. (In the UK it's £11 a month or £84 a year; in Australia it's AU$19 or AU$135.)

Premium: A step up from Extra tier adding in PlayStation 1, PS2, PS3 and PSP games, growing the overall catalog to more than 700 games. That tier is available at $18 a month, or $120 a year. It also has time trial game demos, so subscribers try out certain games for a few hours before buying. (In the UK it's £13.49 a month or £100 a year. In Australia, where it's called "Deluxe" for some reason, it's AU$22 or AU$155.)

As for the games available, they're some of the best on the PlayStation console. This includes Death Stranding Director's Cut, God of War (2018), Demon's Souls (the updated 2020 version), Spider-Man: Miles Morales, Red Dead Redemption 2, Control and Marvel's Guardians of the Galaxy. Those who have the Premium tier will also access classics from older generations, including Dark Cloud 2, Syphon Filter, Tekken 2 and Hot Shots Golf.

Since PS Now included cloud gaming before it was integrated into the new PS Plus, this means game streaming is available from the get go. For Xbox Game Pass, that took years to implement. This means subscribers can play games on their consoles without having to download them or on their PC via the PS Plus app. Some of the classic games are only available to play via streaming, and as long as your internet connection is speedy and stable, there are hardly any noticeable hiccups.

The Xbox Game Pass flavor of cloud gaming, however, lets you play some games on phones and tablets, or laptop web browsers.

The overall PS Plus catalog is larger than Xbox Game Pass, and it offers some unique features. But there are flaws with the service that Sony will need to address if it wants to match the popularity of Microsoft's service.

Read more: Best Games on PS Plus

Some major minuses

PS Plus' biggest issue is the lack of organization with the catalog of games. There are a few categories games are placed in, but there seems to be little rhyme or reason to it. The Xbox Game Pass user interface is similar to what someone would see on Netflix or Disney Plus, by having some of the more notable games and certain genres easily discoverable. PS Plus, on the other hand, doesn't have this so it's just tedious to find something of interest.

Another glaring problem is the overall quality of games. It's not as though you'd expect all 700 games to be winners, but there are some absolute garbage games seemingly there just to pump up the numbers. This was the biggest issue with PS Now, and it carried over to the new PS Plus. Xbox Game Pass, in comparison, has just over 100 games available, but it seems like the games are of a higher overall average quality than what PS Plus has to offer. Compound the lackluster games on top of the lousy UI and finding a new game to play becomes a bit monotonous.

What makes the catalog issue even more frustrating is the lack of certain Sony-published games. Microsoft made it clear that its games will be available on Xbox Game Pass from launch day, and they will stay on there. It's been true for Halo Infinite and Forza Horizon 5, and will be for upcoming games like Bethesda's Starfield.

Sony has yet to do the same with many of its well-known classic games as well as its most recent titles. PS Plus feels like it should include The Last of Us Part 2, Horizon Forbidden West and most of the Gran Turismo titles… but it doesn't.

There's also the question of the longevity of the titles. PS Now routinely had titles available for a few months before they were removed, and it's unclear if PS Plus will do the same.

While cloud streaming is available at launch, there's a lack of platforms available to stream to. There are no apps for iOS or Android, and the PC app, while it works, reportedly has problems with not being able to launch certain games.

PS4 and PS5 owners who want the absolute most bang for their bucks should subscribe to at least the Extra tier of PS Plus. It's still a wealth of great games to play at a reasonable monthly price. Fans of some of the older titles could see a reason to jump to the Premier tier in order to play those classic games, while the Essential tier should be avoided, as it makes little sense to not pay the extra $5 a month to access hundreds of games.

Playstation plus review a great deal that s also a real mess cartoon playstation plus review a great deal that ended playstation plus review artinya playstation plus review a company playstation plus reviews playstation plus discount playstation plus extra

PlayStation Plus Review: A Great Deal That's Also a Real Mess

PlayStation Plus Review: A Great Deal That's Also a Real Mess

Sony's PlayStation Plus subscription game service, originally intended to sell online gaming access, went through a big change in June. Still called PS Plus, it has now become Sony's version of Xbox Game Pass, offering access to a large and evolving Netflix-style catalog of games. While it does some things better than Microsoft, the new PS Plus still lags behind in other aspects of the service.

The new PS Plus offers three subscription tiers, from an Essential package that mimics the old PS Plus, to Extra and Premium tiers offering hundreds of games, cloud streaming, monthly bonus games and online multiplayer access. What it doesn't offer, however, is a clean interface to make it easy to find games, and it also includes only a few of the biggest Sony games on the PlayStation platform. PS Plus mostly lines up with Xbox Game Pass on paper when you're going down a list of features. But for overall value and accessibility, it doesn't always feel like that when actually using it.

PS Plus is a big plus

Before the big update, Sony offered two different PlayStation subscriptions. PS Plus for playing online, with a couple of bonus games every month, was $10. PS Now offered a catalog of mostly older games to download or cloud stream for the same price. The new PS Plus combines the two under a single name and comes in three tiers:

Essential: Same as the original PS Plus, with two or three bonus monthly games, which you keep only as long as you're an active subscriber; online play; cloud saves; and PSN Store discounts. It costs $10 a month, or $60 a year. (In the UK it's £7 a month or £70 a year, and in Australia it's AU$12 or AU$80.)

Extra:All the features of Essential and more than 400 PS and PS5 games available to download or selectively stream. It costs $15 a month, or $100 a year. (In the UK it's £11 a month or £84 a year; in Australia it's AU$19 or AU$135.)

Premium: A step up from Extra tier adding in PlayStation 1, PS2, PS3 and PSP games, growing the overall catalog to more than 700 games. That tier is available at $18 a month, or $120 a year. It also has time trial game demos, so subscribers try out certain games for a few hours before buying. (In the UK it's £13.49 a month or £100 a year. In Australia, where it's called "Deluxe" for some reason, it's AU$22 or AU$155.)

As for the games available, they're some of the best on the PlayStation console. This includes Death Stranding Director's Cut, God of War (2018), Demon's Souls (the updated 2020 version), Spider-Man: Miles Morales, Red Dead Redemption 2, Control and Marvel's Guardians of the Galaxy. Those who have the Premium tier will also access classics from older generations, including Dark Cloud 2, Syphon Filter, Tekken 2 and Hot Shots Golf.

Since PS Now included cloud gaming before it was integrated into the new PS Plus, this means game streaming is available from the get go. For Xbox Game Pass, that took years to implement. This means subscribers can play games on their consoles without having to download them or on their PC via the PS Plus app. Some of the classic games are only available to play via streaming, and as long as your internet connection is speedy and stable, there are hardly any noticeable hiccups.

The Xbox Game Pass flavor of cloud gaming, however, lets you play some games on phones and tablets, or laptop web browsers.

The overall PS Plus catalog is larger than Xbox Game Pass, and it offers some unique features. But there are flaws with the service that Sony will need to address if it wants to match the popularity of Microsoft's service.

Read more: Best Games on PS Plus

Some major minuses

PS Plus' biggest issue is the lack of organization with the catalog of games. There are a few categories games are placed in, but there seems to be little rhyme or reason to it. The Xbox Game Pass user interface is similar to what someone would see on Netflix or Disney Plus, by having some of the more notable games and certain genres easily discoverable. PS Plus, on the other hand, doesn't have this so it's just tedious to find something of interest.

Another glaring problem is the overall quality of games. It's not as though you'd expect all 700 games to be winners, but there are some absolute garbage games seemingly there just to pump up the numbers. This was the biggest issue with PS Now, and it carried over to the new PS Plus. Xbox Game Pass, in comparison, has just over 100 games available, but it seems like the games are of a higher overall average quality than what PS Plus has to offer. Compound the lackluster games on top of the lousy UI and finding a new game to play becomes a bit monotonous.

What makes the catalog issue even more frustrating is the lack of certain Sony-published games. Microsoft made it clear that its games will be available on Xbox Game Pass from launch day, and they will stay on there. It's been true for Halo Infinite and Forza Horizon 5, and will be for upcoming games like Bethesda's Starfield.

Sony has yet to do the same with many of its well-known classic games as well as its most recent titles. PS Plus feels like it should include The Last of Us Part 2, Horizon Forbidden West and most of the Gran Turismo titles… but it doesn't.

There's also the question of the longevity of the titles. PS Now routinely had titles available for a few months before they were removed, and it's unclear if PS Plus will do the same.

While cloud streaming is available at launch, there's a lack of platforms available to stream to. There are no apps for iOS or Android, and the PC app, while it works, reportedly has problems with not being able to launch certain games.

PS4 and PS5 owners who want the absolute most bang for their bucks should subscribe to at least the Extra tier of PS Plus. It's still a wealth of great games to play at a reasonable monthly price. Fans of some of the older titles could see a reason to jump to the Premier tier in order to play those classic games, while the Essential tier should be avoided, as it makes little sense to not pay the extra $5 a month to access hundreds of games.

Inflation interest rates and jobs how today stencile inflation interest rates and jobs how today weather inflation interest rates and jobs howard inflation interest rates and jobs howell inflation interest rates and jobs howey inflation interest rates and jobs howden inflation interest rates and recession inflation interest rate calculator inflation interest rates inflation interest rate relationship jimmy carter inflation interest rates inflation interest rate history

Inflation, Interest Rates and Jobs: How Today's Economy Compares to Recessions of the Past

Inflation, Interest Rates and Jobs: How Today's Economy Compares to Recessions of the Past

This story is part of Recession Help Desk, CNET's coverage of how to make smart money moves in an uncertain economy.

What's happening

There's still debate about whether the US economy is officially headed into a recession, but the economic downturn is causing widespread stress.

Why it matters

Periods of financial volatility and market decline can drive people to panic and make costly mistakes with their money.

What's next

Examining what's happening now -- and comparing it with the past -- can help investors and consumers decide what to do next.

Facing the aftershocks of a rough economy in the first half of 2022, with sky-high inflation, rising mortgage rates, soaring gas prices and a bear market for stocks, leading indicators of a recession have moderated slightly in the past month. That could mean the economic downturn won't be as long or brutal as expected.

Still, the majority of Americans are feeling the sting of rising prices and anxiety over jobs. The country has experienced two consecutive quarters of economic slowdown -- the barometer for measuring a recession -- even though the National Bureau of Economic Research hasn't made the "official" recession call.

At a time like this, we should consider what happens in a recession, look at the data to determine whether we're in one and try to maintain some historical perspective. It's also worth pointing out that down periods are temporary and that, over time, both the stock market and the US economy bounce back.

I don't mean to minimize the gravity and hardship of the times. But it can be useful to review how the economy has behaved in the past to avoid irrational or impulsive money moves. For this, we can largely blame recency bias, our inclination to view our latest experiences as the most valid. It's what led many to flee the stock market in 2008 when the S&P 500 crashed, thereby locking in losses and missing out on the subsequent bull market.

"It's our human tendency to project the immediate past into the future indefinitely," said Daniel Crosby, chief behavioral officer at Orion Advisor Solutions and author of The Laws of Wealth. "It's a time-saving shortcut that works most of the time in most contexts but can be woefully misapplied in markets that tend to be cyclical," Crosby told me via email.

Before you make a knee-jerk reaction to your portfolio, give up on a home purchase or lose it over job insecurity, consider these chart-based analyses from the last three decades. We hope this data-driven overview will offer a broader context and some impetus for making the most of your money today.

What do we know about inflation?

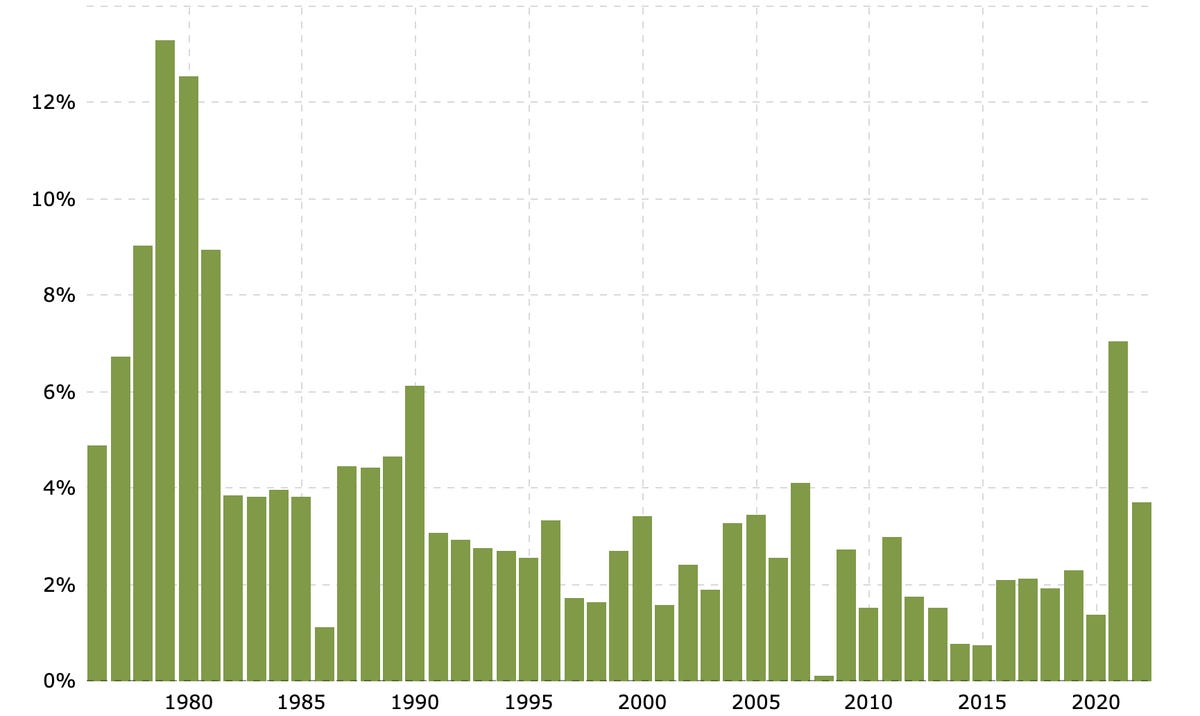

Historical inflation rate by year

Macrotrends.net

Current conditions: The US is experiencingthe highest rate of inflation in decades, driven by global supply chain disruptions, the injection of federal stimulus dollars and a surge in consumer spending. In real dollars, the 8.5% rise in consumer prices over the past year is adding about $400 more per month to household budgets.

The context: Policymakers consider 2% per year to be a "normal" inflation target. The country's still experiencing over four times that figure. The 9.1% annual rate in July was the largest jumpin inflation since 1980 when the inflation rate hit 13.5% following the prior decade's oil crisis and high government spending on defense, social services, health care, education and pensions. Back then, the Federal Reserve increased rates to stabilize prices and, by the mid-1980s, inflation fell to below 5%.

The upside: As overall inflation rates rise, the silver lining might be increased rates of return on personal savings. Bank accounts are starting to offer more attractive yields, while I bonds -- federally backed accounts that more or less track inflation -- are attracting savers, too.

What's happening with mortgage rates?

30-year fixed-rate mortgage averages in the US

Current conditions: As the Federal Reserve continues its rate-hike campaign to cool spending and try to tame inflation, the rate on a 30-year fixed mortgage has grown significantly. In June, the average rate jumped annually by nearly 3 percentage points to almost 6%. In real dollars, that means that after a 20% down payment on a new home (let's use the average sale price of $429,000), a buyer would roughly need an extra $7,300 a year to afford the mortgage. Since then, rates have cooled a bit, even dipping back down below 5%. What happens next with rates depends on where inflation goes from here.

The context: Three years ago, homebuyers faced similar borrowing costs and, at the time, rates were characterized as "historically low." And if we think borrowing money is expensive today, let's not forget the early 1980s when the Federal Reserve jacked up rates to never-before-seen levels due to hyperinflation. The average rate on a 30-year fixed-rate mortgage in 1981 topped 16%.

The upside: For homebuyers, a potential benefit to rising rates is downward pressure on home prices, which could cause the housing market to cool slightly. As the cost to borrow continues to increase with mortgages becoming more expensive, homes could experience fewer offers and prices would slow in pace. In fact, nearly one in five sellers dropped their asking price during late April through late May, according to Redfin.

On the flip side, less homebuyers mean more renters. Rent prices have skyrocketed, and housing activists are asking the White House to take action on what they call a "national emergency."

What about the stock market?

Dow Jones Industrial Average stock market index for the past 30 years

Macrotrends.net

Current conditions: Year-to-date, the Dow Jones Industrial Average -- a composite of 30 of the most well-known US stocks such as Apple, Microsoft and Coca-Cola -- is about 8.5% below where it started in January. Relative to the broader market, technology stocks are down much more. The Nasdaq is off almost 19% since the start of the year.

The benchmark S&P 500 stock index hit lows in June that marked a more than 20% drop from January, which brought us officially into a bear market. Since then, it's bounced back up a little, but some experts warn that a current bear market rally is at odds with expected earnings and we could see even lower stock prices in the near future.

The context: Stock price losses in 2022 are not nearly as swift and steep as what we saw in March 2020, when panic over the pandemic drove the DJIA down by 26% in roughly four trading days. The market reversed course the following month and began a bull run lasting more than two years, as the lockdown drove massive consumption of products and services tied to software, health care, food and natural gas.

Prior to that, in 2008 and 2009, a deep and pervasive crisis in housing and financial services sank the Dow by nearly 55% from its 2007 high. But by fall 2009, it was off to one of its longest winning streaks in financial history.

The upside: Given the cyclical nature of the stock market, now is not the time to jump ship.* "Times that are down, you at least want to hold and/or think about buying," said Adam Seessel, author of Where the Money Is. "Over the last 100 years, American stocks have been the surest way to grow wealthy slowly over time," he told me during a recent So Money podcast.

*One caveat: If you're closer to or living in retirement and your portfolio has taken a sizable hit, it may be worth talking to a professional and reviewing your selection of funds to ensure that you're not taking on too much risk. Target-date funds, a popular investment vehicle in many retirement accounts that auto-adjust for risk as you age, may be too risky for pre- or early retirees.

What does unemployment tell us?

US unemployment rates

Current conditions: The July jobs report shows the unemployment rate holding steady, slightly dropping to 3.5%. The Great Resignation of 2021, where millions of workers quit their jobs over burnout, as well as unsatisfactory wages and benefits, left employers scrambling to fill positions. However, that could be changing as economic challenges deepen: More job losses are likely on the horizon, and an increasing number of workers are concerned with job security.

The context: The rebound in theunemployment rate is an economic hallmark of the past two years. But the ongoing interest rate hike may weigh on corporate profits, leading to more layoffs and hiring freezes. For context, during the Great Recession, in a two-year span from late 2007 to 2009, the unemployment rate rose sharply from about 5% to 10%.

Today, the tech sector is one to watch. After benefiting from rapid growth led by consumer demand in the pandemic, companies like Google and Facebook may be in for a "correction." Layoffs.fyi, a website that tracks downsizing at tech startups, logged close to 37,000 layoffs in Q2, more than triple from the same period last year.

The upside: If you're worried about losing your job because your employer may be more vulnerable in a recession, document your wins so that when review season arrives, you're ready to walk your manager through your top-performing moments. Offer strategies for how to weather a potential slowdown. All the while, review your reserves to see how far you can stretch savings in case you're out of work. Keep in mind that in the previous recession, it took an average of eight to nine months for unemployed Americans to secure new jobs.

§

What's happening

Home prices overall are up by 37% since March 2020.

Why it matters

Surging home prices and higher interest rates make monthly mortgage payments less affordable.

What's next

Rising mortgage rates will make borrowing money more expensive, which will lessen competition to buy homes and eventually flatten prices.

Home prices continued to skyrocket in March as buyers tried to stay ahead of rising mortgage rates.

Prices increased by 20.6% this March compared to last year, according to the S&P CoreLogic Case-Shiller Indices, the leading measures of US home prices. This was the highest year-over-year increase in March for home prices in more than 35 years of data. Seven in 10 homes sold for more than their asking price, according to CoreLogic.

Out of the 20 cities tracked by the 20-city composite index, Tampa, Phoenix and Miami saw the highest year-over-year gains in March. Tampa saw the greatest increase, with an almost 35% increase in home prices year-over-year. All 20 cities experienced double-digit price growth for the year ending in March.

The strongest price growth was seen in the south and southeast, with both regions posting almost 30% gains in March. Seventeen of the 20 metro areas also saw acceleration in their annual gains since February.

"Those of us who have been anticipating a deceleration in the growth rate of US home prices will have to wait at least a month longer," said Craig Lazzara, managing director at S&P DJI, in the release. "The strength of the Composite indices suggests very broad strength in the housing market, which we continue to observe."

Since the start of the pandemic in March 2020, home prices overall are up by 37%. The current surge in home prices is a result of tight competition between buyers in a low-inventory market as they attempt to lock in lower mortgage rates before rates jump even higher throughout the year, as experts predict they will.

If you're considering buying a new home -- or are actively in the market -- the news isn't all bad. Interest rates are at their highest point in more than 40 years, and one potential benefit of that may, eventually, be downward pressure on home prices. As it becomes increasingly expensive to borrow money, fewer people will seek to do so, and homes for sale may receive fewer offers leading to, eventually, lower prices. In fact, nearly one in five sellers lowered their asking price during a four-week period in May and April, according to Redfin.

"Mortgages are becoming more expensive as the Federal Reserve has begun to ratchet up interest rates, suggesting that the macroeconomic environment may not support extraordinary home price growth for much longer," said Lazzara. "Although one can safely predict that price gains will begin to decelerate, the timing of the deceleration is a more difficult call."

Lenovo x1 fold hands on a first step toward the next big idea lenovo x1 fold hands on a first step toward the next big penny lenovo x1 fold hands on a first step toward the next big bitcoin lenovo x1 fold hands on a first step toward loving lenovo x1 fold hands which thumb lenovo x1 fold hands boardmaker lenovo x1 fold youtube lenovo x1 folding laptop lenovo x1 fold

Lenovo X1 Fold hands-on: A first step toward the next big thing in PCs

Lenovo X1 Fold hands-on: A first step toward the next big thing in PCs

"This is the most innovative thing I've seen all year." That was what my wife said when I demoed the Lenovo X1 Fold and all its tricks and extras. She's a former tech and games journalist, so she's seen a thing or two. She's not one to be taken in by hype.

But that reaction is warranted, especially in a year when most of the big product releases were slight upgrades to existing lines, or in the case of Apple's new Macs, a purely internal chip upgrade deliberately designed to be nearly invisible to the user. This, on the other hand, is a real step in a new direction, combining a kitchen sink full of ideas into a new take on the traditional Windows PC.

The Lenovo X1 Fold feels like an updated version of the laptop-tablet two-in-one hybrid.

Dan Ackerman/CNET

Like the Samsung Galaxy Fold or Motorola Razr, the X1's screen is made of a flexible material that can fold in half. Unlike those phones, the big benefit here is not necessarily access to a larger screen, but the ability to set up and use the X1 Fold in a variety of different ways. It's more like an updated version of the classic laptop-tablet two-in-one hybrid than a Windows version of a folding-screen phone.

I actually saw the X1 Fold for the first time back in May 2019, as an early prototype. Even then, it worked well enough, although in the wake of the original Samsung Fold launch debacle, there was a lot of concern about the longevity of folding-screen devices. I saw it again at CES 2020 in January, along with several other interesting new laptop and PC prototypes. But of those, the X1 Fold is the first to actually go on sale, starting at a hefty $2,499 (or five PS5 consoles).

The Lenovo X1 Fold starts at $2,499.

Dan Ackerman/CNET

Having spent a couple of days with the final retail version of the X1 Fold, I can definitively say a few things about it. It is indeed one of the most interesting new tech products of the year. It's also a first-gen product that only the bravest early adopters will want to buy, especially at that price. The accessories (it's an extra $300 to get the stylus pen and Bluetooth keyboard) are a must-have, especially the keyboard, which -- as with the Microsoft Surface Pro -- is the cleverest part of the whole package.

The system has four basic setups that it can jump between. It starts as a 13-inch OLED-screen Windows tablet, powered by a low-power Intel Core i5-L16G7 CPU. It's limited to 8GB of RAM with either 256GB or 512GB storage options.

The outer shell has a leather cover with a built-in kickstand. Turn the tablet to landscape mode, fold out the kickstand and sit the Bluetooth keyboard in front of it, and you've got a mini desktop PC with a 13-inch screen. It feels like using an iPad with a keyboard, especially now that iPadOS supports touchpads.

Lenovo has added a software overlay to control what happens when the system detects you folding the screen.

Dan Ackerman/CNET

But it's when you fold the screen that things start to get interesting. As Windows has no native support for folding-screen devices, Lenovo had to add a software overlay to control what happens when the system detects you folding the screen. A small pop-up menu asks how you'd like the open windows arranged -- split into the top and bottom halves, or full-screen, taking up the whole display. If you choose to send your active window to the top half of the folded screen, you can now pull up the Windows on-screen keyboard on the bottom half and use it to type. Is typing on an on-screen keyboard ever a fantastic experience? No, and that doesn't change here, but I loved the feel of turning a slate-style tablet into a mini laptop.

But wait a minute. Wasn't there a Bluetooth keyboard involved? Can't I use that instead of the on-screen keyboard? Yes, and that's my favorite part of the X1 Fold so far. The thin keyboard is the perfect size to fit over the bottom half of the screen when it's folded into a clamshell shape. In fact, the keyboard attaches via magnets and inductively charges itself when sitting on top of the screen.

The Bluetooth keyboard is my favorite part of the X1 Fold so far.

Dan Ackerman/CNET

No, it's not like typing on a MacBook Air, but it's a big step up from the on-screen keyboard. It even has a small, finicky touchpad built in. Even better, when you fold the screen all the way down, as if closing the lid of a laptop, the keyboard fits perfectly inside, allowing you to carry it easily.

It's all these little clever touches and engineering feats that make this feel more like a promising first-gen product instead of a not-fully-baked prototype.

Here are a few areas where the X1 Fold feels like it still needs some work:

The stylus has nowhere to live except in an elastic strap on the side of the keyboard.

The keyboard's compact design means a lot of layout compromises. Good luck hitting the semicolon, em dash or question mark without hunting.

Like all folding-screen devices, there's a distinct crease in the middle. It's barely visible when the screen is bright, but you can definitely feel it.

The overall design makes a few compromises, with a thick screen bezel and awkward webcam placement.

In slate mode, I was able to fold it like a half-open book and use the Kindle reader app to get one page on each side of the screen but it required messing around in the app settings and still felt awkward as an ebook reader.

I'm currently benchmarking the Lenovo X1 Fold and will report the results soon in an expanded review. In the meantime, I'm enjoying it as a fun end-of-the-year surprise, and it reminds me of what I used to call a "CEO laptop." Something clever and new, but not entirely practical, that your status-obsessed CEO would see and say, "Somebody get me one of those things!"

Getting a new iphone transfer everything getting a new iphone getting a new iphone 8 getting a new iphone 12 getting a new iphone icloud backup what to do when getting a new iphone getting new iphone how to transfer everything getting a new birth certificate getting a new passport getting a new drivers license getting a new puppy getting a new kitten getting a new cat getting a new credit card getting a loan getting a gst number canada getting a mortgage getting a heloc with bad credit getting a job getting a pardon in canada

Getting a new iPhone every 2 years makes less sense than ever

Getting a new iPhone every 2 years makes less sense than ever

We all know the drill. As Apple's annual fall event draws close, many of us start to check in on our previous two-year smartphone plan to see if we're eligible for an upgrade in September. After all, the newest phone is only the newest phone for so long. Even for discerning shoppers like me, it takes serious willpower to resist the lure of a purple iPhone or 1TB of storage.

Mobile carriers have long persuaded many of us to upgrade our smartphones every two years, offering two-year contracts linked to free or low-cost phone upgrades to keep the two-year upgrade cycle going. That feeling of ponying up just a couple hundred dollars (or less) for the newest, fanciest phone available has helped perpetuate the rise of the de facto two-year phone upgrade. Case in point: AT&T and Verizon marketed a "free" iPhone 12 last year for customers who buy unlimited plans and commit to a multiyear deal. And the trade-in deals were even better this year for the iPhone 13.

But even though that might still be the norm in the US, a routine upgrade isn't a thing for much of the world.

I was born and raised in developing Asia, a region where buying a smartphone is financially unattainable for hundreds of millions of people, much less a two-year upgrade. In India, the average person needs to save two months' salary to buy the cheapest available smartphone, according to a survey published by the Alliance for Affordable Internet last August. From my perspective, the trend of routinely upgrading a phone every two years when it doesn't change that much is a privilege, one that reminds me of the stark income equality gap as well as the ever-increasing digital divide globally.

Read more:Billions of people still can't afford smartphones: That's a major problem

Beyond that, and perhaps more tangibly, I think we should consider the environmental cost of purchasing a new phone. You've read the headlines: Climate change is accelerating at rapid speed. Countries around the world keep setting new records for the highest temperatures. There are more climate-related disasters than ever before, arctic caps are melting and biodiversity is disappearing faster than we can save it. What, exactly, happens to all those discarded phones over time? Does all that plastic ever fully decompose?

Apple says it removed the in-box charger from its iPhone 12 lineup for environmental reasons.

Apple

Read more:Apple is opening up its world of iPhone recycling

Consumer electronics are responsible for tonnes of e-waste annually, which in turn contributes to the climate crisis. Experts have warned about how e-waste disposal contributes to climate change due to the chemicals released when the waste is burned, some of which are equivalent to carbon dioxide.

For years, developed countries like the US have shipped recyclable waste overseas for processing. Although that is now beginning to change, there are real costs. iPhones contain toxic materials like lead and mercury, for instance, which can harm the environment and people if disposed of improperly. And often e-waste isn't properly managed. In Southern China, there is a town called Guiyu that has become known as the world's biggest graveyard for America's electronic junk, and synonymous among environmentalists with toxic waste. The UN's 2020 Global E-waste Monitor report found that the world dumped a record 53.6 million tonnes of e-waste last year, of which the US is the world's second-largest contributor to e-waste, dumping 6.9 million tonnes.

Read more:I paid $69 to replace my iPhone battery: Here's what happened

While Apple is committed to a net zero supply chain by 2030, it's tough to argue that there's a better alternative to lower carbon consumption than less consumption. After all, Apple says the iPhone 12's end-to-end supply chain emits 70 kilograms of carbon to the atmosphere. If even 1 million people waited that extra year, we could save 70,000,000 kilograms of carbon from going into the air in a year. Imagine if it was 10 million or 100 million. It's something to think about before making that upgrade.

The smartphone upgrade cycle has gotten longer

Even with the enticing deals offered by carriers, the upgrade cycle has seemingly lengthened. In recent years, several reports show how Americans and Europeans are more than happy to hold on to their phones for longer periods of time. In fact, in 2019 smartphone upgrades hit record lows at two of the biggest US carriers, Verizon and AT&T. Carriers like T-Mobile and Verizon seem to have responded to this by offering month-to-month plans, which offer more flexibility and options, indicating a potential departure from the "norm" of a two-year phone upgrade.

Barring big-picture factors like the struggling global economy amid the ongoing pandemic as well as our increased mindfulness over the environment, I think this trend is persisting for a confluence of reasons. Phones today are receiving software, and therefore security, updates for longer. For instance, 2015's iPhone 6S is compatible with iOS 15, potentially dampening desires for a bi-yearly upgrade.

In addition to all this, smartphone innovation has hit a plateau, and the industry bears the hallmarks of one that's maturing: slowing smartphone sales growth along with the slower evolution of what we need, what we want and so forth. There are no big surprises here: Today's phones are getting more nice-to-have refinements rather than the awe-inspiring innovation seen just three or four years ago.

Decreasing technological gap

Up until a couple of years ago, smartphone manufacturers had us sitting on the edge of our seats, waiting for the next design refresh. But that's not as much the case anymore. With the iPhone 12 series, 5G was probably its buzziest feature -- one that understandably ended up triggering an upgrade supercycle. But the most exciting thing for many of us at CNET was MagSafe, which is hardly new. Apple's proprietary technology, allowing you to magnetically snap on attachments, was first introduced some 15 years ago with the first-gen MacBook Pro. It was then reintroduced for the iPhone 12.

Patrick Holland/CNET

When you look at what changed from the iPhone 11, you'll see the usual suspects on your list: 5G, OLED screen, new design. Admittedly there are a few more things you won't see everywhere, such as MagSafe and the Ceramic Shield, but nothing extra-special to truly write home about. Personally, the last time I was blown away by an iPhone reveal was back in 2017 when Apple introduced the iPhone X, which set new design standards for the modern-day iPhone. The iPhone X did away with the physical home button and chunky bezels of its predecessors and made way for a sleek, futuristic device that inspired the iPhone 12 family. Also, for the first time with Apple, we were able to unlock an iPhone with Face ID, Apple's facial recognition technology.

Looking at the iPhone 13, the narrative sounds familiar. We knew it wouldn't get a major technical upgrade (though that didn't stop us from wishing). While we appreciate the upgrades Apple did give the phone (a smaller notch, a larger battery and a faster screen refresh rate), the iPhone 13 is "not radically different," according to CNET's Patrick Holland. Plus a number of these new iPhone features, like the 120Hz screen, currently exist on Android phones, reinforcing the notion of a decreasing technological gap in the smartphone landscape. Apple itself says the life-cycle of a typical iPhone is now three years. So the company times its new releases accordingly: We get a major redesign every three years, not two, with more minor updates in between.

Look no further than the glitziest non-Apple flagship launch of this year for clues: Samsung's Galaxy S21 family. Here the standout change wasn't made to the hardware or software, but perhaps to its least interesting feature: its price tag. The S21 lineup has a starting price of $800 (£769, AU$1,249), which is $200 less than last year's $1,000 Galaxy S20, making for an enticing deal.

Apart from that, major differences between the S21 and last year's S20 were mostly incremental. I remember having to pore over the specs sheet to spot salient differences as I covered Samsung's virtual Unpacked event. Refinements were made to the usual suspects, including the processor, software and 5G. This might have been part of Samsung's response to the global coronavirus pandemic, but again it lends credence to the notion of that decreasing technological gap. It was also interesting to note the items Samsung dropped from the S21 flagship family to meet that lowered price. We said goodbye to expandable storage, bundled earphones and most notoriously the in-box charger, as Samsung followed in Apple's lead -- apparently in the name of the environment.

Read more: Here's what we know so far about Samsung's Galaxy S22

Let's also take a moment to consider the question: What makes the S21 an attractive buy? Chances are, a great camera, fast performance, battery longevity and a crisp display with narrow bezels are at the top of your list. But the truth is 2019's Galaxy S10 boasts all those features. Heck, even the Galaxy S7 from five years ago did. My point is yearly changes have become too incremental to compel most people to upgrade with urgency, especially given the backdrop of rising smartphone prices.

Samsung's Galaxy Z Flip.

Angela Lang/CNET

Are we at peak phone?

I'm not discounting foldable phones. Samsung and Huawei have made undeniable technological progress, and their bendy handsets have dramatically altered the way smartphones are used and could represent the future of the industry. But folding phones are far from the mainstream. Phone manufacturers and carriers in the US have moved the most innovative devices to a price that's simply beyond reach for most people. For instance, the Galaxy Fold 3 starts at $1,800 (£1,599, AU$2,499) and Huawei's Mate X2, available in China for now, costs nearly $3,000 ($2,800, £1,985, AU$3,640 converted). Until these prices hit price parity with, say, the iPhone 12 Pro or Pro Max, foldable phones are likely to remain a niche product.

Smartphone innovation has stagnated, and this is not a knock against the consumer electronics companies or the tech giants that design them. Maybe we've reached peak smartphone, and this is as far as it needs to go. It could well be part of the reason why the race to upgrade your phones is slowing.

Ipad mini review an excellent 2021 upgrade but still a niche definition ipad mini review an excellent 2021 upgrade but still a niche market ipad mini review an excellent 2021 upgrade buttstock ipad mini review an excellent 2021 upgrade usb ipad mini review an excellent 2021 upgrade magnetic mini ipad mini review an excellent 2021 form ipad mini review an excellent 2021 chevy ipad mini review an excellent wife ipad mini review and reinforce ipad mini sale

iPad Mini review: An excellent 2021 upgrade, but still a niche tablet

iPad Mini review: An excellent 2021 upgrade, but still a niche tablet

What's the most improved product in Apple's lineup this year? It might be the sixth-gen iPad Mini. The company's smallest tablet got the makeover I thought it needed years ago: Now it has the iPad Air's better display, a USB-C port instead of Lightning, a much better processor and better cameras too. You can also magnetically snap an Apple Pencil right onto the side now. Pretty great, huh?

iPad 9th gen vs. iPad Mini 9th gen

iPad 9th gen 2021

iPad Mini 2021

Screen size

10.2 inches

8.3 inches

CPU

A13 Bionic

A15

Starting storage

64GB

64GB

Rear camera

8MP Wide camera

12MP Wide camera

Connector

Lightening

USB-C

Broadband option

4G LTE

5G

Apple Pencil support

1st gen

2nd gen

Weight

1.07 pounds

0.65 pound

Starting price

$329

$499

The only problem is, the iPad Mini isn't a must-have gadget. Far from it; as much as the iPad is usually a secondary device for many people, the iPad Mini is often a second iPad. Which makes this a luxury for most. But the 8.3-inch screen, A15 Bionic processor (same as the iPhone 13) and excellent overall performance could make it a first choice for some, and the $499 (£479, AU$49) starting price, while high, isn't as absurdly high as other Apple products.

iPad Minis aren't as necessary with large phones nearby. And the Mini can't do the one thing larger iPads do very well: connect with keyboard cases easily to become sort-of laptops.

But if you think you'll want an iPad that can be an e-reader and gaming device and casual TV screen and sketch pad and notebook and smart home screen, with some email and social media stuff thrown in, this is a pretty lovely choice. If you're OK with its higher-than-basic-iPad but lower-than-iPad-Pro price, that is.

The Mini has grown on me the more I've used it. And really, all of its features seem upgraded, making for a lovely, speedy little tablet. But I won't be doing any serious writing on it. And with iPhones, more affordable iPads and flashy but still-evolving foldable devices all doing what this Mini does (and possibly better), you have to consider this Mini an overdue revamp that's unnecessary for most. Some will absolutely love it, though.

I'm going to stop trying to type on this Mini, and go back to my laptop to continue this review.

iPad Mini, iPad Air, iPad Pro 12.9-inch: a progression of sizes.

Scott Stein/CNET

It's really small... and growing on me

As I take the iPad Mini out of its box, I think to myself, Oh, this really is small. I'm not sure I like that. After using a larger 12.9-inch iPad Pro recently, this iPad feels extremely tiny. Too tiny. I get used to it, though.

The size of this iPad lines up much more with the folding-phone-phablet-Kindle-Switch landscape. It's more of a relaxed handheld. It feels fine held in one hand, and it's easy to carry around in a pinch. It's got a smaller footprint than the 2019 iPad Mini, in fact, but it's also a bit thicker. The Mini comes in new colors now, but they're very very subtle. Mine is purple, but the matte aluminum finish looks more like a slight variation of gray.

And while that small size could be appealing to some people as a bigger-than-a-phone-smaller-than-most-iPads thing, it also makes using it as a laptop replacement really hard.

The iPad Mini next to the iPhone 12 Pro. The iPad Mini is definitely bigger than that.

Scott Stein/CNET

You can pair a keyboard with Bluetooth, but there's no dedicated keyboard case (maybe Logitech or others will make one). And the usable screen space gets even smaller when you use the onscreen keyboard to type.

You'll also need a brand-new cover, since no older Mini ones fit. The Mini uses magnets on the back so that a wraparound folio cover snaps right on, but like the iPad Pro and iPad Air cases, that won't provide any drop protection.

But yes, this is bigger than an iPhone. It's still significantly bigger than an iPhone 12 Pro (more than twice the size), and I have to admit, I'm carrying it around for reading and games a lot more than I was expecting. But these days, I'm still mostly carrying it around the house.

I stood it up (using the sold-separately smart cover) on my back porch table while putting together a Weber charcoal grill, and called up the instruction manual. It was better than using a phone, but I also thought… hmm, a regular-size iPad would be easier to read.

In the last few days, I've started taking it everywhere. I took it to the doctor's office even though I have a phone. Why? I like the extra screen. I guess it's why people like big folding phones, too.

The iPad Mini's squared-off corners and USB-C port, next to the ninth-gen iPad's older Lightning port.

Scott Stein/CNET

USB-C and a new design, at last

The design of this iPad is completely revamped, much like the iPad Air last year. The flat edges, the sharper screen, the better stereo speakers, a USB-C port, a side magnetic charge strip where second-gen Pencils can snap onto and a side Touch ID home button… this is the total makeover I wanted in the 2019 iPad Mini. I love the look, and it makes me want to use the iPad, even if I'm not interested in using a Mini. It woos me. It all looks great.

But it's not perfect. The repositioned volume buttons on the top edge of the iPad feel weird, though maybe they make more sense when watching videos in landscape mode. And the bezels, while smaller, are still very noticeable to me. They become even more noticeable when using certain apps (see below).

The iPad Mini 2019 (left) versus iPad Mini 2021: Videos look bigger with less bezel.

Scott Stein/CNET

A new aspect ratio means larger videos, but some apps don't benefit

Playing a few games from Apple Arcade, comparing side by side with the 2019 iPad Mini, I think: Wait, does this new iPad display look smaller?

The 8.3-inch, 2,266x1,488-pixel display is a longer display than the 2019 iPad Mini's. It also has slightly rounded corners like the rest of the iPad Pro and Air line. Apple says in the fine print that "actual viewable area is less" than the diagonal measurement. Also, apps that haven't been updated for this new screen size will be pillar boxed with subtle black bars, making the bezels seem bigger and the display seem effectively the same (or even slightly smaller) than the 2019 Mini's. Since this is a prerelease of the Mini, Apple Arcade games currently have black bars, for instance. Safari and Notes and other core apps don't. Some apps will autoadjust, and others will need developers to adapt them (as for previous iPads with different screen sizes).

Documents and things like comics don't always end up looking bigger (iPad Mini 2021 on the left, iPad Mini 2019 on the right).

Scott Stein/CNET

PDFs, graphic books and digital magazines, which often have 4:3 document layouts, also don't take advantage of the larger screen area. It's just a reminder that the "bigger screen" isn't really what it seems to be here.

But it helps for videos, which play in a wider aspect ratio already. There's a bit less letterboxing, and videos fills a larger area of the screen.

A15 performance: Very good

The A15 processor in the Mini is like the one in the new iPhones. Think of it as a hybrid of older iPad Pros and more recent iPhones. The single-core Geekbench 5 benchmark score average I got was 1,598, which is similar to the iPhone 12 models' scores last year. But the multicore score is 4,548, which is close to what Apple's pre-M1 iPad Pros could handle with the more graphics-boosted A12Z chip. Like pretty much every current-gen Apple device, the 2021 iPad Mini is fast enough that you won't have to worry about taxing the system, at least with currently available apps.

Two apps at once can feel small sometimes, but it's almost like two phone screens glued together, too.

Scott Stein/CNET

Multitasking: Mostly works

Holding the Mini sideways with two apps open, it first feels cramped. Then I realize this is close to the two-app split view that the Microsoft Surface Duo has, or that folding phones like the Fold can do. It's kind of like two phone screens side by side, except you can't fold the Mini.

I wanted to hate how small the Mini is, but I'm starting to find multitasking on an 8-inch screen kind of addictive. It's exactly what the iPhone can't do. iPadOS 15 makes swapping apps in and out of multitasking mode a bit easier, but the tiny triple-dot icon on the top of the screen is also easy to accidentally press in some apps, since it's near a lot of top menu bars and icons.

The iPad Mini camera with flash (middle) compared with the iPad 9th gen (left) and the lidar/dual-camera iPad Pro (right).

Scott Stein/CNET

Rear camera with flash, and digital-zoom wide-angle front camera

The Mini's cameras are good: not recent iPhone-level, but more than good enough. A rear flash and 4K video recording will make it good enough for documentation or on-the-spot videos and photos, though it doesn't have multiple rear cameras, and doesn't have lidar scanning like the iPad Pro models do. The front camera has a wider-angle mode that taps into Apple's digital-zooming Center Stage tech, which debuted on the iPad Pro in the spring. It's helpful for face-following while on video chats using FaceTime, Zoom and other supported apps, and is a feature that all Apple devices should add.

So many devices, and the Mini feels a bit like so many of them.

Scott Stein/CNET

Game console? E-reader? Sketchpad? Sure. But… pricey

The size of this Mini sets it up as a gaming tablet, or a Kindle alternative, or a very nice superportable sketchpad. This is what Apple is clearly leaning into with the Mini. There's also a business audience for a revamped and faster mini tablet for point-of-sale or field work.

But add up what this will cost: $499 only gets you 64GB of storage and a USB charger in the box. Buy a case, which you'll absolutely need ($60) and that nice Pencil ($130), and upgrade the storage to 256GB ($150) and you're at $840. Not cheap!

The Microsoft Surface Duo (left) and the new iPad Mini (right). A future glimpse, perhaps, at where the iPad's size could go next...

Scott Stein/CNET

Could this be a phone? Not really

It's tempting. The new Mini has 5G (but read the fine print on that one). It's small. It's sort of lower-priced than iPhones. But there are clear downsides. It's not water-resistant or drop-resistant like an iPhone. It's large, like really large -- you'd need a big jacket pocket or a bag. It doesn't have GPS. There's no actual phone call app. And I don't know why it took me so long to realize, but iPads have no haptics, which is weird. No buzzing for silent notifications, and no subtle feedback in games and in apps.

It really makes me think about using a 5G-enabled iPad Mini as a phone replacement. Apple has a clear gap in its product lineup. The Mini feels like the sort of device that folding phone makers are aiming toward. The Mini is the best option Apple has in that space. But a future iteration could end up being the candidate for a folding display, like the Microsoft Surface Duo or the Samsung Galaxy Fold 3 (which, by the way, both cost a lot more than an iPad Mini).

About that 5G: The Mini's flavor of 5G doesn't support the limited-availability but sometimes very fast millimeter-wave frequency like the iPhone 12 and 13 and the spring iPad Pro do. If you don't know what I'm talking about, 5G signals come in several types, and mmWave (where available) is like a very fast local hotspot. This means, effectively, that this Mini's 5G won't reach superhigh speeds. In suburban Montclair, New Jersey, my Verizon 5G test SIM speeds ranged from 270Mbps to 170Mbps, which is basically similar to LTE. The $150 cellular modem add-on plus monthly fee isn't worth it to me (but maybe your business will foot the bill?)

Using it while putting together a charcoal grill. Second grill, second iPad.

Scott Stein/CNET

It's nice, but niche

I just bought a charcoal grill, a Weber. I already have a gas grill. Why did I do this? I wanted an affordable one that could do charcoal, too. Sometimes people buy second grills. It's a luxury, and a niche. People buy second things. Or specialized things. The Mini is a great total revision, but I wouldn't say it's a must-have… and it's far too expensive (and limited) for kids. (Or my kids, anyway.) For your family, maybe, it might be worth the upgrade if you're in love with the design and don't mind the mini size. But it's the best iPad Mini, if you ever craved one and have the cash to spend. It's a lovely little luxury.