What to expect from the housing market in 2022: Another sellers' market

This story is part of The Year Ahead, CNET's look at how the world will continue to evolve starting in 2022 and beyond.

The last 22 months have been some of the wildest in real estate history, as the COVID-19 pandemic accelerated the speed and intensity of recent trends. Home prices surged to record-breaking highs. Interest rates dropped to historic lows. And, amongst it all, the new era of online home buying and selling took further root. On top of that, just about every contemporary macro-economic trend -- from inflation to supply chain woes to labor shortages -- made an appearance in the 2021 housing market, increasing the advantages of existing homeowners, daunting prospective homebuyers and, ultimately, further widening wealth inequality in the US.

Though no one can predict what the next year will bring, we've asked some industry experts to help us read the tea leaves. Perhaps most significantly, home prices are expected to continue to rise, though at a slower rate than last year. As such, the 2022 housing market will present challenges for new buyers looking to get a foothold. For those looking to sell, new technologies like iBuying will continue to streamline and simplify real estate transactions. And existing homeowners will likely have another year to capitalize on rising property values through refinancing -- if they haven't already.

Experts also predict an extension of two major 2021 trends: low housing inventory and supply chain issues, both of which will continue to hamstring construction and renovations. Meanwhile, there are two new spectres on the scene: inflation and rising interest rates. "For a homebuyer, 2022 is going to require patience and strategy," said Robert Dietz, chief economist the National Association of Home Builders.

"If you think you're going to wait on the sidelines for the market to cool off, that usually doesn't work," cautions Karan Kaul, senior research associate at the Urban Institute. "Timing" the market is a tricky enterprise, and prices seem unlikely to decrease meaningfully any time soon.

With the caveat that political and virological developments can wreak havoc on this unpredictable corner of the economy, here are some of the major factors experts see influencing the housing market in 2022.

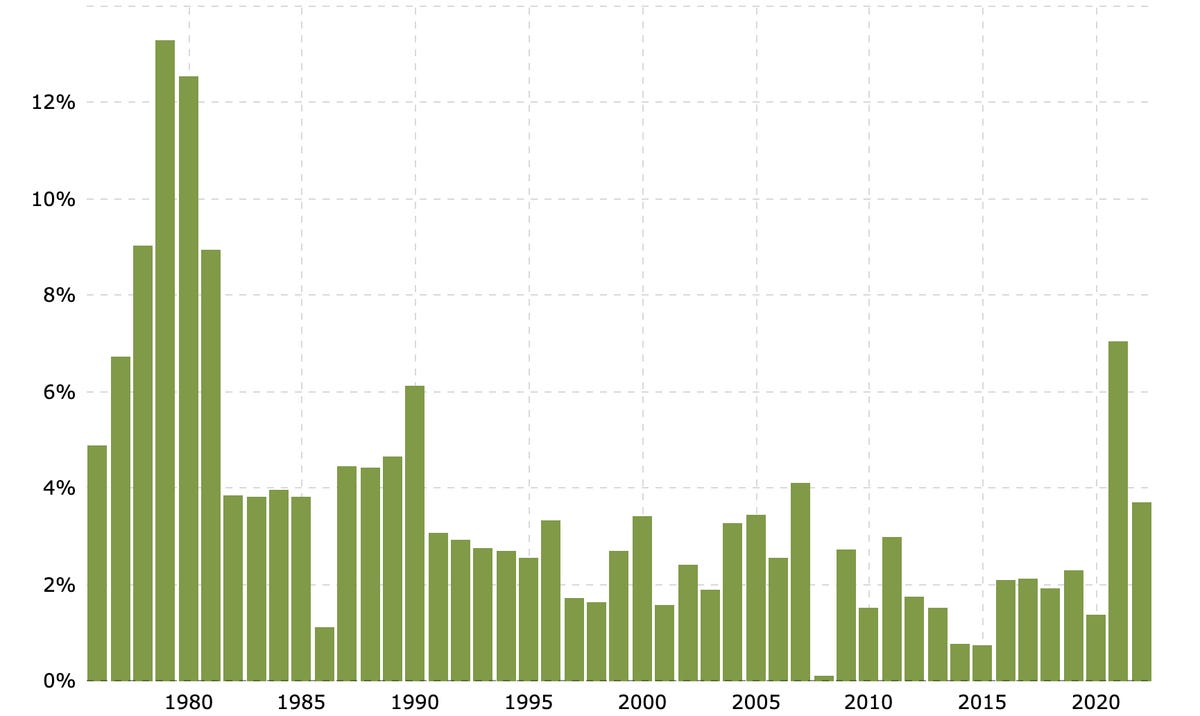

Still smoking: Home prices continue to rise

If you already own a home, you're more than likely to be in a fortunate position. Skyrocketing home values have continued to increase equity for homeowners in many US regions throughout the pandemic, according to Dietz.

Combined with historically low interest rates, a record-breaking number of homeowners were able to tap into their home equity in 2020. As property values surged during the first year of the pandemic, cash-out refinancing levels were at their highest since the 2007 financial crisis.

Of course, this creates a much more difficult situation for prospective homebuyers. And that's unlikely to change much in 2022. Although prices are expected to increase at a lower rate next year, they are expected to continue to rise. And that -- in addition to higher interest rates -- will create considerable headwinds for buyers throughout 2022.

Clogged supply chains cause more delays

Supply chain disruptions caused by the COVID-19 pandemic continue to delay shipments which impedes new construction. That is only making the market that much more competitive along with the rising price of existing homes across the US. And the number of people looking to buy is also increasing, thanks in large part to millennials entering the housing market in growing numbers.

"We've seen so much interest in buying homes over the past year and a half, it's a bit difficult to project when that is going to lose some steam," according to Robert Heck, vice president of mortgage at Morty, a mortgage-tech start-up. But it's clear there are still plenty of buyers trying to enter the market despite prices continuing to creep up.

"Despite the fact that builder confidence is pretty strong right now, in the short run there is a lack of building materials, higher cost of building materials like lumber, appliances, windows and doors, and even garage doors," said Dietz. And further complicating the picture is a sustained labor shortage, particularly for skilled construction workers.

Delivery delays can extend build time by as much as four to eight weeks for a typical single family home. And if there aren't enough contractors on hand to use those materials once they show up, it's clear that demand will continue to outweigh supply for some time to come.

Macro headwinds: Interest rates and inflation

Prospective homebuyers will want to keep their eyes on some wonky stuff in 2022. The Federal Reserve announced that it will wind down bond purchasing and look to raise interest rates next year. And higher interest rates will only make things more difficult for those looking to buy, as they raise both the average monthly payment and the total lifetime cost of a mortgage.

And don't forget about inflation! That will almost certainly increase both the cost of home building materials and skilled labor. In fact, the National Association of Realtors' anticipates that annual median home prices will increase by 5.7% in 2022.

And yet it's not all doom and gloom. Mortgage interest remains are still quite low. And there are pockets of affordability in many regions of the US, creating a key opportunity for those fortunate enough to be able to work remotely.

"Mortgage rates are still at historical lows, and it's been harder than ever to predict where things are going thanks to the ongoing COVID-19 pandemic," said Heck.

Tech innovations reshape home buying

Digital lending has already impacted the way Americans shop for homes. The rapid rise of online real estate brokerages and mortgage marketplaces has made it easier than ever to browse properties and finance a home. That's unlikely to change: Almost 40% of millennials said they would feel comfortable buying a home online in a recent Zillow study.

"Consumers like the ability to bid remotely, and to really take a look at properties and neighborhoods online," said Miriam Moore, division president of default services at ServiceLink, a mortgage transactional services provider. This will likely impact both sides of transactions, as sellers learn to adapt their home's curb appeal to someone looking at it on their phone and buyers (and agents and investors) look for ways to arbitrage the market.

An evolving challenge: Climate change

Perhaps the biggest unknown in real estate is how soon climate change will become the dominant factor. According to experts across the industry, every part of the homebuying process will eventually be affected by changing weather patterns, encroaching shorelines, shifting flood zones and an increasingly complicated insurance marketplace. Case in point: Moore, who is in the mortgage business, has seen an increase in inspections due to weather and fire over the last year.

New construction may prove to be both more energy efficient and more durable in the face of extreme weather. "People want to live in energy efficient homes, but they can only buy them if they exist," said Kaul, at The Urban Institute.

The stakes couldn't be higher. Buying a house remains one of the most reliable ways to build wealth and has long been a key milestone for Americans in establishing long-term financial security. And although interest rates remain as low as ever, given all of the other trends impacting the real estate market in 2022, the balance of power is likely to remain in the hands of sellers.

Source

Tags:

- Housing Market What To Expect In 2021

- What To Expect When Building A House

- What Does Housing Do

- What To Expect From Therapy

- What To Expect From The Autumn Statement

- What To Expect From The New Iphone

- What To Expect From The Psat

- What To Expect From The Class

- What To Expect From Radiation Treatment

- What To Expect When You Re Expecting